What Is BaaS, And What’s Its Role Inbuilding Mobile Banking?

April 26, 2025

In today’s rapidly evolving financial landscape, Banking-as-a-Service (BaaS) emerges as a transformative business model. By seamlessly connecting existing banks, including digital and traditional institutions, with non-banking businesses that utilize embedded finance, BaaS enables a direct integration of payment processing and access to a bank’s system through application programming interfaces (APIs). In this article, we delve into the remarkable utility of BaaS and its potential to revolutionize the way businesses manage their financial operations.

What Is Banking As A Service (BaaS)?

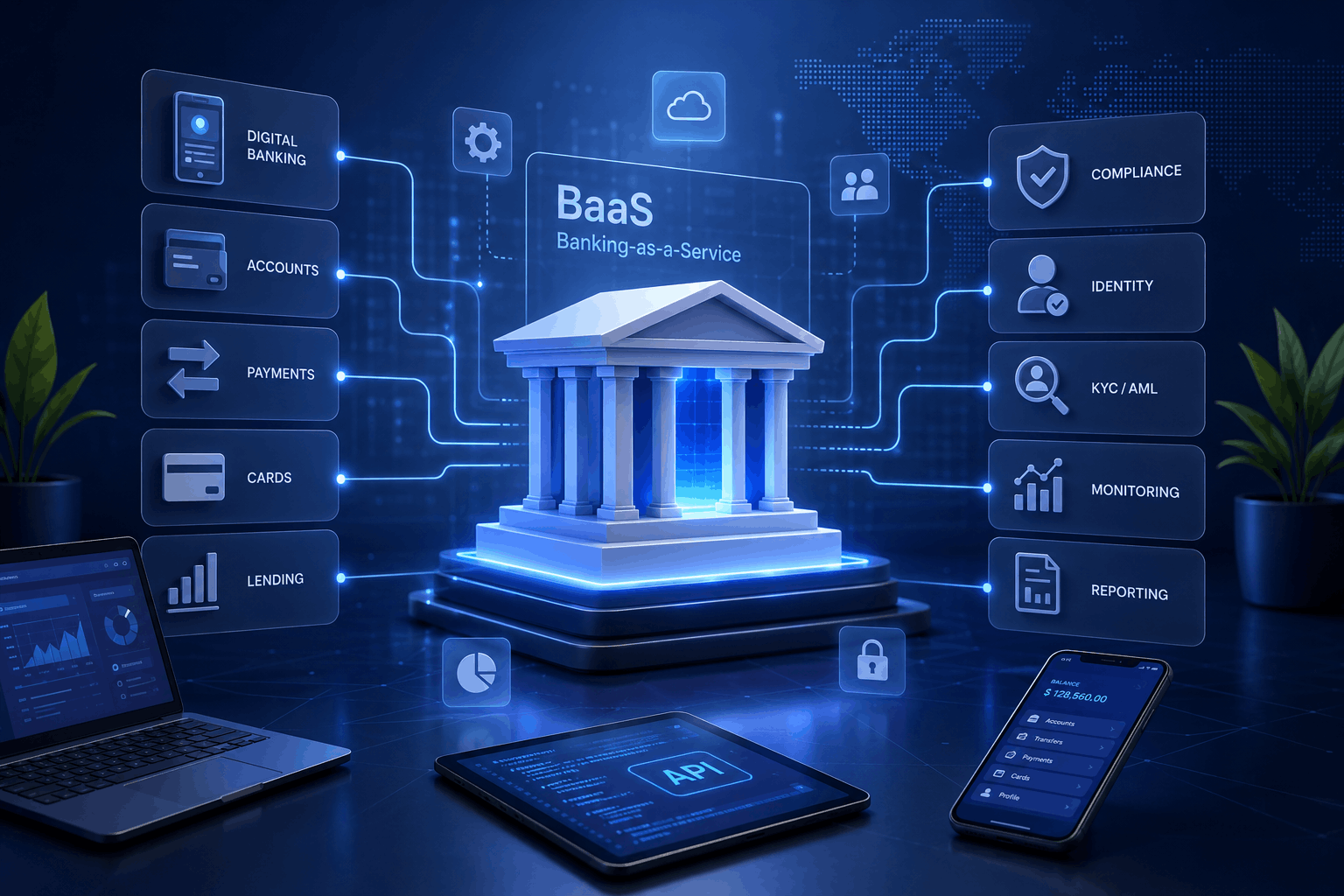

BaaS is an end-to-end solution that allows both licensed financial institutions and businesses without banking licenses to offer comprehensive financial services such as providing digital bank accounts, credit access, payment services, virtual and physical cards and tailored financial products. Banking as a service eliminates the need to establish banking operations or rely on third-party financiers, enabling businesses to offer licensed financing solutions. It empowers banks and fintech companies to create user-friendly digital platforms, granting consumers access to a wide range of banking services. As a result geographical barriers are eliminated, fostering financial inclusion. BaaS bridges the gap between banks, non-banking entities, and consumers, unlocking financial services and enhancing accessibility.

How Does It Work?

To fully experience BaaS, three key components are required: authorized financial institutions, BaaS providers, and fintech brands. The licensed bank lends its license to the provider, who facilitates communication through APIs with the bank’s infrastructure. This brings a secure and regulated financial framework, along with compliance and customer information. The provider then offers comprehensive solutions for integrating financial services, including user interface design, products, risk evaluation, account management, that can be integrated by fintech companies. They in turn provide their end-clients with access to banking functionalities and leverage BaaS capabilities to enhance their products and deliver a seamless customer experience.

BaaS platforms democratize access to banking products, allowing non-financial companies to leverage open banking APIs and provide core services traditionally offered by banks. BaaS tools empower tech-savvy financial institutions and non-financial companies to modernize the customer experience. By incorporating embedded finance and other features, businesses can aggregate various services into a single banking platform, expanding customer channels and revolutionizing the way financial and banking offerings are distributed.

Regardless of the chosen BaaS solution, ensuring the highest level of security is crucial. Robust security measures should be implemented at every level to protect sensitive financial data. For more information, refer to our comprehensive guide on security options for fintech app development.

Benefits of Banking as a Service

Banking as a Service (BaaS) brings significant advantages to all stakeholders. Final consumers benefit from improved user experiences with faster transactions, convenient payment options, and online loan approvals. Brands/businesses that are using integrated finance/BaaS solutions within their platforms experience increased customer loyalty, additional revenue generation, and reduction of infrastructure costs. Fintechs enjoy a competitive edge by delivering financial solutions swiftly and cost-effectively without requiring a banking license, leveraging seamless data flow with BaaS. BaaS providers can capitalize on transaction fees and contribute to industry progress by fostering innovative fintech app ideas. And finally, financial institutions increase profits through provider commission fees and additional revenue streams and facilitates data flow, enabling them to gain valuable consumer insights for personalized offerings.

What are the Challenges?

Implementing a Banking as a Service (BaaS) model comes with its fair share of challenges. Overcoming these obstacles is crucial to providing user-friendly financial solutions. Lets highlight some of the most crucial of them.

Bringing Traditional Banks Up to Date: Most traditional banks use outdated systems that are incompatible with modern technologies, making integration of third-party services challenging. BaaS can drive the need for a more updated architecture and facilitate the exposure of services through APIs.

Shifting Functions of Key Players: Collaboration with multiple third-party players in BaaS may lead to confusion among customers. A detailed and elaborated onboarding process is required to reduce possible shortcomings in product delivery, ongoing operations and maintenance.

Complexity of API Integration: Developing a robust API strategy is not easy, as organizations face challenges in exposing operational processes and maximizing business value. Focus should be on ease of integration and minimizing cumbersome integration factors. Standardization of API approaches may shape the future of the finance industry.

While there are challenges to overcome in implementing BaaS, solutions are emerging to address them. Upgrading traditional banking systems, adapting to shifting roles of players in the financial industry, and developing a well-defined API strategy are essential steps. As technology progresses, the evolution of the BaaS model and possible solutions that address these obstacles in the coming years will be intriguing to observe.

Selecting the Right Provider for Your Business

Choosing the ideal Banking-as-a-Service (BaaS) provider can be a daunting task due to the variety of vendors and offerings available.

Currently the most typical BaaS configurations that can be found on the market are:

- BaaS Providers: They offer comprehensive banking software solutions, licenses, products, operations, and/or technology to aggregators, banks, and non-financial companies (NFCs).

- Providers-Aggregators: These entities combine BaaS capabilities with other vendors, providing a complete “out-of-the-box” solution to end customers.

- Distributors: They leverage consumer behavior insights and customer relationships to curate a unique suite of banking services.

- Distributor-Aggregators: These entities enhance their distributed propositions by incorporating new products or technology from multiple providers.

Selecting the right BaaS provider is crucial for integrating banking solutions successfully. By understanding the various BaaS configurations and considering factors such as alignment with business needs, scalability, integration capabilities, regulatory compliance, track record, pricing, security, and support, businesses can make informed decisions and pave the way for growth and implementation success. Therefore the following steps should be taken before making your final decision:

- Evaluate how well the provider’s offerings align with your business requirements and goals, including banking software, product, and operational needs.

- Assess the provider’s ability to accommodate your business growth and evolving customer demands, ensuring their technology and operations support your long-term objectives.

- Consider the provider’s seamless integration with your existing systems and platforms, enabling a streamlined customer experience.

- Verify the provider’s adherence to necessary regulatory standards and compliance requirements, ensuring the security and privacy of customer data.

- Research the provider’s past projects, portfolio, and customer reviews to gauge their reliability and level of service.

- Understand the provider’s pricing structure, conduct a comprehensive financial analysis, and compare costs with competing firms to assess value and ROI.

- Evaluate the provider’s security measures and protocols to protect sensitive customer data, ensuring alignment with industry standards and compliance requirements.

- Consider the level of technical support, response times, and communication channels provided by the BaaS provider.

Banking-as-a-Service (BaaS) Market Size and Forecast

The Banking-as-a-Service (BaaS) market is experiencing rapid growth driven by evolving customer demands and the adoption of innovative financial solutions. Approximately 30% of clients are contemplating changing their banking relationship, reflecting growing dissatisfaction with traditional banking products and services. This shift in customer sentiment presents an opportunity for BaaS providers to attract new customers by offering more innovative and customer-centric solutions. Moreover, as consumer preferences evolve, 42% of consumers have utilized “Buy Now, Pay Later” services at some point, demonstrating the increasing popularity of flexible payment options. Banks that focus on BaaS offerings have experienced significant benefits, with a reported 2X Return on Average Assets (ROAA). By leveraging BaaS capabilities, banks can expand their service portfolio, tap into new revenue streams, and provide value-added solutions to customers.

The banking-as-a-service market is witnessing significant growth, driven by customer dissatisfaction with traditional banking models, the popularity of flexible payment options, and the financial benefits for banks focusing on BaaS. As the market continues to evolve, there are abundant opportunities for BaaS providers to cater to changing customer demands, enhance profitability, and shape the future of the financial industry.

Top BaaS Platform Providers

Numerous companies have already successfully adopted the BaaS model. Here are some of the institutions offering embedded finance and other services in this sphere:

- Modulr – a fintech company that provides Payments as a Service API for digital businesses. It enables users to automate payment flows, embed payments into the platform, and build new payment products and services themselves from a single API. Modulr has direct access to the Bank of England and claims to facilitate a fast experience that digital customers demand. The company was founded in 2015 and is headquartered in London, England.

- Striga (formerly Lastbit) provides financial services infrastructure for companies in the crypto, banking & issuing space. This platform is a product that evolved as a cumulative effort of the Lastbit line of products launched operated throughout 2019 and 2020, which was the first ever physical instant Bitcoin powered debit MasterCard on the planet. With increasing demand for the platform powering the Lastbit applications, Striga aims to solve this problem for the hottest new FinTechs that wish to embed crypto-banking into their applications.

- Railsr – a financial services company. They provide the creation of digital ledgers, connecting digital ledgers to bank accounts, receiving money, sending money, converting money, issuing cards, and managing credit through the API that enables banks and corporate customers to transact digitally.

How Finhost can help with BaaS?

In today’s digital era, the demand for Banking as a Service (BaaS) providers has grown significantly, as businesses across industries seek streamlined banking and financial solutions. Selecting the right BaaS provider can be a challenging task, given the multitude of options available. That’s where FinHost comes in bridging the gap between customer’s end-users needs and selecting an optimal BaaS provider. As a leading technology consultancy specializing in cloud infrastructure, FinHost offers assistance in picking the perfect banking provider tailored to the unique requirements of businesses. Through in-depth assessment, market research, and provider evaluation, FinHost ensures that only the most reliable and competent BaaS providers are considered. Moreover, our personalized recommendations, guided by factors like project size, budget constraints, and technology stack, streamline the decision-making process. With an extensive expertise and ongoing technical support, FinHost ensures a smooth implementation and integration, enabling businesses to maximize the benefits of their chosen BaaS solution. Choose FinHost Company to navigate the BaaS landscape with confidence and unlock the full potential of your banking infrastructure.