Core Banking Systems: Architecture, Types and Components

April 23, 2026

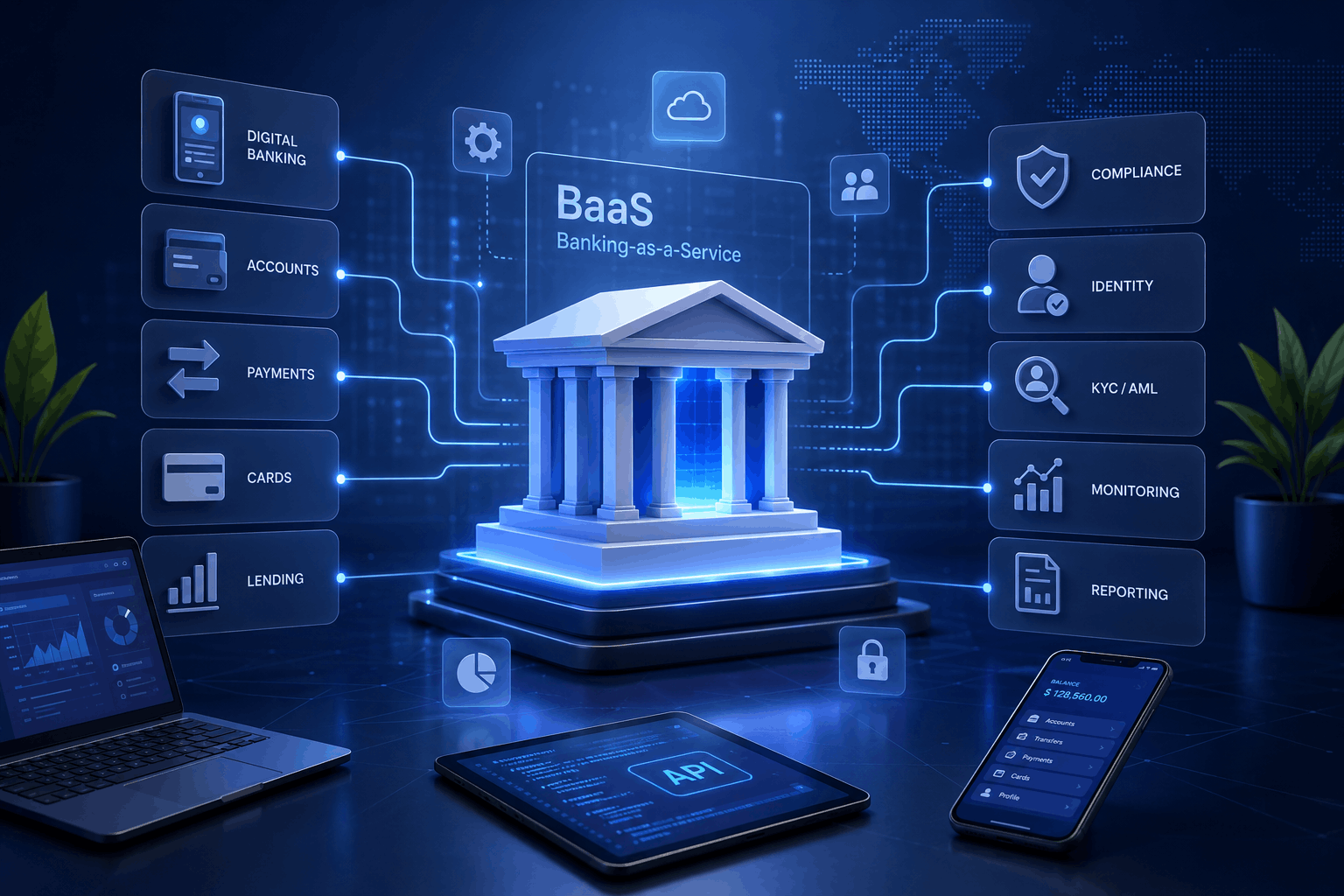

Core banking systems are the operational backbone of modern financial products, enabling real-time transaction processing, account management, and seamless integration with payment networks, compliance providers, and third-party services.

In 2026, core banking is no longer just a backend system for traditional banks — it has evolved into a modular, API-driven infrastructure powering neobanks, fintech platforms, embedded finance products, and crypto-enabled services.

A modern core banking platform typically includes a central ledger, payment processing engine, compliance layer (KYC/AML), and an integration hub that connects to external providers such as card issuers, payment rails, and liquidity partners.

For fintech companies, choosing the right core banking system is one of the most critical decisions, directly impacting time-to-market, scalability, regulatory compliance, and long-term product flexibility.

This guide explains how core banking systems work, their architecture and key components, the different types available today.

What Is a Core Banking System (Beyond Definition)

A core banking system is not just a backend platform that processes transactions — it is the operational foundation on which modern financial products are built.

Traditionally, core banking systems were designed to support internal bank operations such as account management, transaction processing, and ledger maintenance. These systems operated as closed, monolithic infrastructures, primarily focused on stability rather than flexibility.

Today, this paradigm has fundamentally changed.

In 2026, a core banking system functions as a modular, API-driven infrastructure that enables financial institutions and fintech companies to build, launch, and scale digital financial products. It acts as the central coordination layer between customer-facing applications, financial operations, compliance processes, and external service providers.

Rather than being a standalone system, modern core banking connects multiple layers of a financial product:

- customer lifecycle management (onboarding, KYC, account setup)

- money movement (payments, cards, FX)

- compliance and risk monitoring

- integrations with external providers (payment rails, card issuers, AML services, liquidity providers)

This shift reflects a broader transformation in the financial industry — from traditional banking systems to composable financial infrastructure.

Core banking is now used not only by banks, but also by:

- neobanks and digital-first financial institutions

- fintech startups launching payment or wallet products

- embedded finance platforms integrating financial services into non-financial products

- crypto and hybrid finance platforms combining fiat and digital assets

In this context, the core banking system becomes a critical enabler of speed and innovation. It determines how quickly a company can launch, how easily it can integrate with partners, and how effectively it can adapt to regulatory and market changes.

As a result, choosing a core banking system is no longer just a technical decision — it is a strategic one that directly impacts product architecture, operational scalability, and long-term business growth.

Core Banking Architecture (How It Really Works)

Modern core banking systems are no longer monolithic platforms: they are modular, API-driven architectures designed to support real-time financial operations, scalability, and seamless integrations. At a high level, a core banking system acts as the central processing layer that connects customer interfaces, financial logic, and external service providers into a single operational ecosystem.

A typical architecture consists of several interconnected layers:

Core Ledger (The Financial Source of Truth)

At the heart of any core banking system is the core ledger: the component responsible for storing and updating all financial data. It manages account balances, transaction records, fees, and internal financial logic. Every transaction flows through the ledger, ensuring consistency and real-time accuracy across the system.

Payment Processing Layer

This layer handles the execution of financial transactions, including SEPA, SWIFT, FPS, internal transfers, and card payments. It connects the core system to external financial networks and providers, often through integrated payment infrastructure solutions that enable access to regulated payment rails and financial ecosystems.

Compliance & Risk Layer

A critical part of modern core banking is the compliance layer, which ensures that all operations meet regulatory requirements. In practice, this includes KYC (identity verification), AML monitoring, transaction screening, and fraud detection. Additionally, these capabilities are typically enabled through pre-integrated KYC and AML solutions, allowing fintech companies to remain compliant without building these systems from scratch. As a result, businesses can reduce implementation time while maintaining regulatory standards.

Integration Layer (API & Provider Ecosystem)

The integration layer is what transforms a core banking system into a fintech-ready platform. Specifically, it enables connections to payment providers, card issuing platforms, FX and liquidity providers, and compliance services. Because it is built on an API-first architecture, this layer allows companies to rapidly expand functionality without rebuilding the system. Furthermore, businesses can add new providers as their needs evolve. In many modern solutions, this is delivered through a unified infrastructure like the FinHost ecosystem, where multiple providers are pre-connected and ready to use. Consequently, fintech companies can launch new financial services much faster while minimizing integration complexity.

Frontend Layer (Web & Mobile Applications)

This layer includes customer-facing applications such as mobile banking apps, web dashboards, and admin panels. These interfaces interact with the core system via APIs, providing users with real-time access to financial services through customizable white-label web and mobile banking apps that significantly reduce development time.

How These Layers Work Together

To understand how this architecture operates in practice, consider a simple payment flow:

- A user initiates a transaction via a mobile app

- The request is sent through the API layer to the core system

- The system checks compliance rules (KYC/AML)

- The payment is routed via an external provider

- The core ledger updates the balance in real time

- The result is returned to the user interface

This modular structure allows financial companies to scale efficiently, integrate new services quickly, and adapt to changing regulatory requirements without rebuilding their entire infrastructure.

Key Components of a Core Banking System

While core banking systems are often described as a collection of individual modules, in practice they function as a structured ecosystem of interconnected components that manage the entire lifecycle of a financial product. Instead of viewing these components separately, it is more effective to group them into functional layers that reflect how financial services actually operate.

Customer Lifecycle Management

This layer is responsible for onboarding users and managing their accounts throughout the entire customer journey. It includes:

- user registration and onboarding

- identity verification (KYC)

- account creation and management

Modern fintech products rely heavily on automated onboarding flows powered by integrated compliance services. For example, many platforms use KYC and AML integrations to verify users in real time while maintaining regulatory compliance.

Money Movement Infrastructure

This component handles how money moves within the system and across external networks. It includes:

- payment processing (SEPA, SWIFT, FPS, local rails)

- internal transfers

- card issuing and transaction handling

- currency exchange (FX)

To enable these capabilities, core banking systems must integrate with multiple providers and payment networks. In practice, this is often achieved through pre-built infrastructure or partnerships, such as white-label financial platforms that already include payment and transaction capabilities.

Financial Core (Ledger & Accounting)

At the center of the system is the financial core, which ensures accuracy, consistency, and transparency of all operations. It includes:

- general ledger

- transaction accounting

- balance management

- financial reporting

This component ensures that every operation — from payments to fees — is correctly recorded and reconciled in real time.

Compliance and Risk Management

Compliance is not a separate feature — it is deeply embedded into every operation within a core banking system. This layer includes:

- AML monitoring

- transaction screening

- fraud detection

- regulatory reporting

Modern platforms integrate compliance directly into transaction flows, ensuring that every action is validated before execution. This reduces risk and simplifies regulatory audits.

Integration & API Infrastructure

One of the most critical components of modern core banking is the integration layer. It enables:

- connections to payment providers

- card issuing systems

- liquidity and FX providers

- external fintech services

API-first architecture allows financial companies to scale and adapt quickly by plugging into external services instead of building everything internally. Platforms like FinHost simplify this process by offering pre-integrated ecosystems and reducing the complexity of managing multiple vendors.

Frontend & User Experience Layer

Although often overlooked in technical discussions, the frontend layer plays a crucial role in delivering financial services to end users. It includes:

- mobile banking applications

- web interfaces

- admin dashboards

These interfaces connect to the core system via APIs and provide real-time access to financial operations. Many companies accelerate development by using white-label mobile banking solutions that are already connected to core infrastructure.

How These Components Work Together

These components do not operate in isolation — they form a unified system where every action triggers multiple processes across layers. For example:

- onboarding triggers KYC checks and account creation

- a payment triggers compliance validation, provider routing, and ledger updates

- reporting aggregates data from all system components

This interconnected structure is what enables modern financial products to operate in real time, scale efficiently, and remain compliant across multiple jurisdictions.

How Core Banking Systems Work

At its core, a core banking system operates as a central processing engine that coordinates every financial action — from user onboarding to real-time transactions and reporting. While the architecture behind it may seem complex, the actual flow of operations follows a structured and repeatable logic.

Example 1: User Onboarding Flow

When a new user registers in a financial application, multiple core banking components are activated simultaneously:

- The user submits registration data through a web or mobile interface

- The system sends the data to the core banking platform via API

- Identity verification is performed using integrated KYC and AML services

- Once verified, a new account is created in the core ledger

- The user gains access to their account via the frontend application

This entire process can happen within minutes in modern systems, enabling fintech companies to onboard users quickly while remaining compliant.

Example 2: Payment Processing Flow

A typical transaction involves several coordinated steps across the system:

- A user initiates a payment in a mobile or web app

- The request is sent to the core banking system via API

- The system performs compliance checks (AML, transaction screening)

- The payment is routed through external providers using integrated infrastructure

- The core ledger updates the account balance in real time

- The transaction result is returned to the user interface

In many cases, this process is supported by external financial networks accessed through payment infrastructure solutions, allowing companies to operate within regulated ecosystems without building connections from scratch.

Example 3: Card Transaction Flow

Card payments involve additional layers of interaction:

- A user makes a payment using a physical or virtual card

- The transaction request passes through card networks (e.g., Visa, Mastercard)

- The issuing provider communicates with the core banking system

- The system validates the transaction and checks available balance

- The ledger updates the account and records the transaction

- The user receives confirmation instantly

These capabilities are often delivered through integrations with card issuing providers and embedded into platforms like white-label financial applications.

Real-Time Synchronization Across the System

One of the key advantages of modern core banking systems is real-time data synchronization. Every action — whether onboarding, payment, or card transaction — is instantly reflected across:

- user interfaces

- internal systems

- reporting tools

- compliance monitoring

This ensures consistency, transparency, and a seamless user experience.

Why This Matters for Fintech Companies

Understanding how core banking systems work is not just a technical detail — it directly impacts business performance. A well-designed system allows companies to:

- launch products faster

- reduce operational complexity

- ensure compliance by design

- scale without rebuilding infrastructure

This is why modern fintech companies increasingly rely on integrated platforms that combine core banking, compliance, and infrastructure into a single ecosystem rather than building each component independently.

Types of Core Banking Systems

Core banking systems can be categorized in different ways, but in practice, most decisions come down to a few key models based on architecture, deployment, and implementation approach. Understanding these types is essential for choosing the right platform for your business.

1. Legacy vs Modern Core Banking Systems

Legacy Core Banking Systems

These systems are traditional, monolithic platforms typically used by established banks. They are characterized by: rigid architecture, limited flexibility, high maintenance costs, and slow integration with new technologies. While these systems are stable, they are not designed for rapid innovation or modern fintech use cases.

Modern Core Banking Systems

Modern systems are built using modular, API-first architecture and are designed to support digital products from day one. As a result, they offer real-time processing, scalability, seamless integration with third-party providers, and support for mobile and digital-first experiences. In addition, their flexible architecture makes it easier to introduce new financial services as business needs evolve. Therefore, fintech companies can innovate faster without rebuilding their infrastructure. Consequently, most fintech companies today rely on modern infrastructures or white-label core banking platforms to accelerate development, reduce technical complexity, and shorten time to market.

2. On-Premise vs Cloud-Based Core Banking

On-Premise Systems

These solutions are hosted on internal infrastructure and fully controlled by the financial institution. They provide maximum control over data and custom security configurations. However, they also require: high upfront investment, dedicated IT teams, and ongoing maintenance.

Cloud-Based Core Banking

Cloud-based systems are now the standard for fintech and digital banking. They offer: faster deployment, lower infrastructure costs, scalability on demand, automatic updates, and improvements. Most modern platforms, including solutions like cloud-based digital banking applications, are built to operate entirely in cloud environments.

3. Build vs Buy vs White-Label

This is one of the most important distinctions when choosing a core banking system.

In-House (Build)

Building a core banking system internally gives full control over the product. However, it comes with: long development timelines (12–24 months+), high costs, and significant technical complexity. This approach is typically used only by large institutions with extensive resources.

Vendor-Based (Buy)

Buying a core banking system from a vendor reduces development time and provides access to pre-built functionality. However, customization can be limited, integrations may still require effort, and vendor lock-in is possible.

White-Label Core Banking Platform

White-label solutions provide a ready-to-launch infrastructure that includes core banking, integrations, and frontend applications. They allow companies to: launch faster, reduce development costs, and access pre-integrated providers.

Platforms like white-label fintech applications combine core banking, payments, compliance, and user interfaces into a single ecosystem, making them especially attractive for fintech startups and companies entering the financial space.

Choosing the Right Type

While all of these types have their place, the industry trend is clear:

- legacy → being phased out

- on-premise → replaced by cloud

- build → replaced by modular or white-label approaches

Today, most fintech companies choose solutions that allow them to launch quickly, integrate easily, and scale without rebuilding infrastructure.

Build vs Buy vs White-Label: Which Core Banking Approach to Choose

One of the most critical decisions when launching a financial product is how to approach your core banking infrastructure. In practice, companies choose between three main options: building a system in-house, purchasing a solution from a vendor, or using a white-label platform.

| Approach | Time to Launch | Cost | Flexibility | Complexity | Best For |

|---|---|---|---|---|---|

| Build (In-House) | 12–24+ months | Very High | Maximum | Very High | Large banks, funded fintechs |

| Buy (Vendor Solution) | 6–12 months | High | Medium | Medium | Mid-size institutions |

| White-Label Platform | 2–4 months | Low–Medium | High | Low | Startups, fast-scaling fintech |

Each approach comes with trade-offs in terms of time, cost, flexibility, and risk.

Build: Full Control, Maximum Complexity

Building a core banking system from scratch provides complete control over architecture, features, and integrations. However, this approach is resource-intensive and slow. Challenges include:

- hiring and managing a large engineering team

- building integrations with payment networks and providers

- implementing compliance (KYC/AML) from scratch

- ensuring security, scalability, and reliability

In most cases, companies underestimate both the cost and the time required to build a production-ready financial system.

Buy: Faster Start, Limited Flexibility

Purchasing a core banking system from a vendor reduces development time and provides access to pre-built modules. This approach allows companies to:

- avoid building infrastructure from scratch

- rely on vendor expertise

- accelerate initial deployment

However, limitations often arise in:

- customization

- integration flexibility

- dependency on vendor roadmap

As a result, companies may still face challenges when scaling or adapting their product.

White-Label: Speed + Flexibility

White-label core banking platforms combine the advantages of both approaches. They provide ready-made infrastructure while maintaining a high level of flexibility through APIs and modular architecture.

With white-label core banking platforms, companies can:

- launch within weeks instead of months

- access pre-integrated providers (payments, cards, KYC)

- reduce development and operational complexity

- focus on product, growth, and user experience

This model is increasingly used by fintech startups, neobanks, and even traditional companies entering financial services.

What Most Companies Choose in 2026

The industry trend is clear:

- building from scratch is becoming less common due to high cost and long timelines

- vendor solutions are still used but can limit flexibility

- white-label and modular platforms are becoming the dominant approach

This shift is driven by the need for faster time-to-market, easier integrations, and the ability to scale without rebuilding infrastructure.

Cloud vs On-Premise Core Banking

When selecting a core banking system, one of the first architectural decisions companies face is whether to deploy it on-premise or in the cloud. While both models are still in use, they represent fundamentally different approaches to building and scaling financial infrastructure.

On-premise systems are typically associated with traditional financial institutions. They provide full control over infrastructure and data, which historically has been important for regulatory and security reasons. However, this control comes at a cost. Maintaining internal infrastructure requires significant investment, dedicated engineering teams, and long deployment cycles. As a result, innovation tends to be slower, and scaling operations becomes more complex.

Cloud-based core banking systems, on the other hand, are designed for flexibility and speed. They allow financial companies to launch faster, scale dynamically, and continuously update their systems without heavy operational overhead. This is why most modern fintech products — including cloud-based digital banking solutions — are built entirely in the cloud.

Today, the industry has largely moved in one direction. While on-premise infrastructure remains relevant for legacy institutions, cloud-based systems have become the default choice for companies that prioritize speed, scalability, and global reach.

Key Challenges in Core Banking Implementation

Despite the technological progress in core banking, launching and scaling a financial product remains a complex task. The challenge is not just in choosing a system, but in orchestrating everything around it.

One of the most demanding aspects is regulatory compliance. Financial services operate in a highly controlled environment where requirements are constantly evolving. Companies must ensure that onboarding, transaction monitoring, and reporting are aligned with frameworks such as PSD2, upcoming PSD3, and AML regulations. This is why many teams avoid building compliance systems internally and instead rely on pre-integrated solutions like KYC and AML services, which significantly reduce both risk and implementation time.

Another major challenge lies in integrations. A core banking system does not function in isolation — it needs to connect with payment networks, card issuing providers, liquidity partners, and compliance tools. Managing these integrations individually can quickly become overwhelming, especially when each provider has its own requirements and technical constraints.

Scalability adds another layer of complexity. As transaction volumes grow, systems must maintain performance without compromising reliability. This requires not only strong infrastructure, but also a well-designed architecture that can handle real-time operations at scale.

At the same time, companies face constant pressure to launch quickly. Time-to-market has become a decisive factor in fintech, and delays in development or integration can directly impact competitiveness. Balancing speed, compliance, and technical quality is one of the hardest challenges in building financial products.

Ultimately, most of these challenges stem from fragmentation. The more components a company builds or integrates independently, the more complexity it has to manage. This is why the market is gradually moving toward unified platforms that reduce this operational burden.

Solutions like FinHost combine core banking, compliance, and integrations into a single ecosystem, helping companies move from idea to launch significantly faster.

If you need guidance on choosing the right architecture or launching your financial product, you can reach out to our team by filling out a short form contact us.

- It was very good document that is for my work. Actually I have started the work in Axos bank project a few month ago. And I was looking for the doc that is for understanding the full workflow of the fintech. It was very big help. Nicholas Sery 06.07.2026 06:32 amReply :