How to Build a Banking-as-a-Service Platform in 2026

July 10, 2026

Banking-as-a-Service has become one of the most important infrastructure models in modern financial services. What began as a way for fintech startups to access banking capabilities through APIs has evolved into a strategic growth model used by banks, electronic money institutions, payment institutions, embedded finance providers, and digital asset businesses.

Banking-as-a-Service continues to expand rapidly as financial institutions and technology companies increasingly adopt API-driven financial infrastructure. According to recent market research, the global BaaS market is projected to exceed USD 1 trillion in 2026, with continued double-digit annual growth expected throughout the decade.

At the same time, the market has become significantly more complex. Launching a Banking-as-a-Service platform today requires far more than connecting payment rails or issuing virtual accounts. Financial institutions must onboard customers across multiple jurisdictions, comply with increasingly demanding regulatory frameworks, support sophisticated organizational structures, and deliver seamless digital experiences while maintaining operational efficiency.

Many organizations entering the BaaS market assume that technology is the primary challenge. In reality, technology is only one part of the equation. The larger challenge lies in designing an architecture that can support compliance, onboarding, account management, payment orchestration, operational controls, and institutional client management simultaneously.

The industry itself has become significantly more demanding. Following increased regulatory scrutiny of Banking-as-a-Service programs in recent years, financial institutions now face much higher expectations around governance, third-party oversight, compliance controls, and operational resilience than during the first wave of BaaS adoption.

The institutions that succeed are not those with the largest number of integrations. They are the ones that build scalable ecosystems where every component works together. In 2026, Banking-as-a-Service is no longer a product. It is an operating model.

This article explores the architecture behind modern Banking-as-a-Service platforms, examines the most common implementation mistakes, and explains why institutional relationship management is becoming one of the most important capabilities in the next generation of financial infrastructure.

Why Most Banking-as-a-Service Projects Fail

Despite strong market demand, many Banking-as-a-Service initiatives struggle to achieve commercial success. Some projects fail before launch, while others encounter operational bottlenecks, compliance challenges, or infrastructure limitations as they scale.

Interestingly, these failures are rarely caused by technology itself.

One of the most common mistakes is treating Banking-as-a-Service as a payment project. Organizations often begin by selecting payment providers and integrating payment rails before defining how the broader platform will operate. Payments are undoubtedly important, but they represent only one layer of a much larger ecosystem. A platform that lacks effective onboarding, compliance workflows, customer management capabilities, and operational controls will eventually struggle regardless of how sophisticated its payment infrastructure may be.

Another common mistake is viewing compliance as something that can be added after launch. Modern financial infrastructure does not work this way. Compliance influences almost every stage of the customer lifecycle, from onboarding and verification to transaction monitoring and reporting. Institutions that delay compliance planning often find themselves redesigning processes, increasing operational costs, and slowing customer acquisition.

A third challenge emerges as organizations begin serving increasingly complex customer structures. Traditional customer management systems were designed for individual customers or standalone businesses. Modern financial institutions frequently serve holding companies, subsidiaries, regional entities, agent networks, and white-label partners operating across multiple jurisdictions. Managing these relationships through disconnected customer records creates duplicated onboarding processes, fragmented compliance reviews, and limited visibility into organizational risk.

Finally, many organizations focus on technology before defining their operating model. Infrastructure decisions should support business strategy rather than determine it. Before selecting providers or designing workflows, institutions should understand who they serve, which markets they target, how they intend to generate revenue, and what regulatory framework will govern their operations.

The most successful Banking-as-a-Service providers start with architecture, not integrations.

The Modern Banking-as-a-Service Architecture

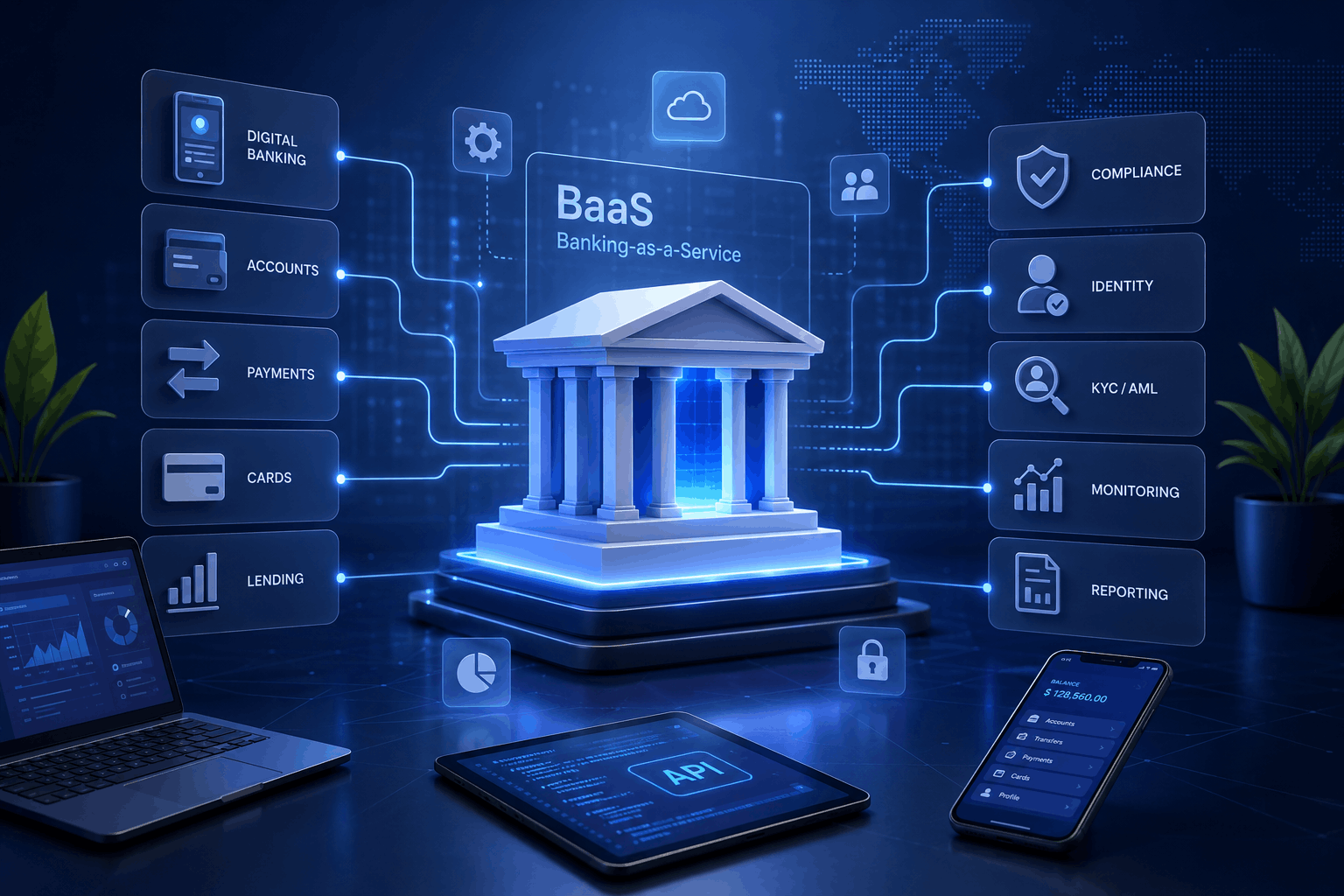

Modern Banking-as-a-Service platforms are no longer built around a single banking system. Instead, they consist of multiple interconnected layers that collectively create a scalable financial ecosystem.

A successful architecture combines customer channels, operational management, compliance controls, banking infrastructure, payment connectivity, and third-party services within a unified framework. Each layer serves a distinct purpose while supporting the broader operational model.

Modern BaaS Platform Architecture

Many organizations underestimate how many interconnected components are required to operate a successful Banking-as-a-Service platform. Payment processing represents only one element within a much larger ecosystem.

Customer-facing applications such as web banking platforms, mobile applications, partner portals, and embedded finance experiences form the visible layer of the platform. Beneath these interfaces sits the API layer, which coordinates communication between services and ensures security, authentication, monitoring, and scalability.

The customer management layer acts as the operational center of the platform, supporting onboarding, permissions, account structures, and lifecycle management. Increasingly, institutions are introducing dedicated relationship management capabilities that allow them to understand how organizations, subsidiaries, agents, and partners connect to one another.

Compliance operates as a continuous infrastructure layer rather than a standalone function. Modern compliance systems support onboarding, monitoring, risk scoring, investigations, and reporting throughout the entire customer lifecycle.

At the foundation of the platform sits the core banking infrastructure responsible for accounts, balances, transaction processing, and financial records. Payment connectivity provides access to domestic and international payment rails, while external service providers contribute specialized capabilities such as identity verification, card issuing, foreign exchange services, and communication tools.

This architectural evolution reflects a broader industry shift toward composable financial infrastructure. Rather than relying on monolithic banking platforms, financial institutions increasingly combine specialized providers for payments, onboarding, compliance, digital identity, treasury, and customer lifecycle management into a unified ecosystem.

Key Takeaway

The most successful Banking-as-a-Service providers no longer think in terms of individual products. They think in terms of ecosystems.

A scalable architecture enables institutions to launch new products faster, onboard customers more efficiently, expand into new markets, and support multiple business models without rebuilding core infrastructure. The ability to orchestrate multiple layers within a unified framework has become one of the defining characteristics of successful Banking-as-a-Service platforms.

Customer and Institutional Onboarding

Customer onboarding is often described as the first step in launching a Banking-as-a-Service platform. In reality, it is much more than that. Onboarding establishes the foundation for compliance, risk management, operational efficiency, and customer experience throughout the entire lifecycle of the relationship.

Many institutions focus heavily on account creation and payment functionality while underestimating the importance of onboarding architecture. This approach often creates challenges later, particularly when customer volumes increase or business models become more complex.

A modern Banking-as-a-Service platform must support several distinct customer categories. Individual customers typically require identity verification, risk assessment, and ongoing monitoring. Business customers introduce additional requirements related to company verification, beneficial ownership checks, and corporate documentation. Institutional customers add another layer of complexity, often involving multiple legal entities, subsidiaries, operational branches, and various user roles operating under a single organizational structure.

As organizations scale, onboarding ceases to be a simple registration process. It becomes a mechanism for collecting, validating, and organizing information that will later support compliance decisions, operational workflows, and customer relationship management.

Regulatory expectations also reinforce this approach. The European Banking Authority (EBA) emphasizes that customer onboarding, governance, and third-party service arrangements should be designed as part of a broader risk management framework rather than as isolated operational processes. This is particularly important for payment institutions and electronic money institutions that rely on multiple technology providers to deliver regulated financial services.

The most successful financial institutions design onboarding as an integrated component of the broader platform architecture rather than a standalone workflow.

Why Traditional Customer Management Breaks Down

Many legacy customer management systems were designed around a simple assumption: one customer equals one record. This assumption no longer reflects how modern financial institutions operate.

Consider a typical Banking-as-a-Service customer. A payment institution may onboard a holding company that owns several subsidiaries operating in different countries. Each subsidiary may have its own directors, beneficial owners, operational teams, and transaction flows. Some may share compliance documentation, while others require separate reviews.

From a regulatory perspective, these organizations are connected. From a risk perspective, they are connected. From an operational perspective, they are connected. Yet many systems continue to treat them as entirely separate customers.

This creates a number of challenges. Compliance teams may repeatedly collect the same documentation. Risk teams may struggle to understand exposure across the broader group. Operations teams may lack visibility into how organizations are related. Customer support teams may find themselves managing multiple disconnected records that actually belong to the same business ecosystem.

As Banking-as-a-Service providers expand into enterprise and institutional markets, these inefficiencies become increasingly difficult to manage.

This is one of the reasons why institutional relationship management is emerging as a strategic capability rather than an operational feature.

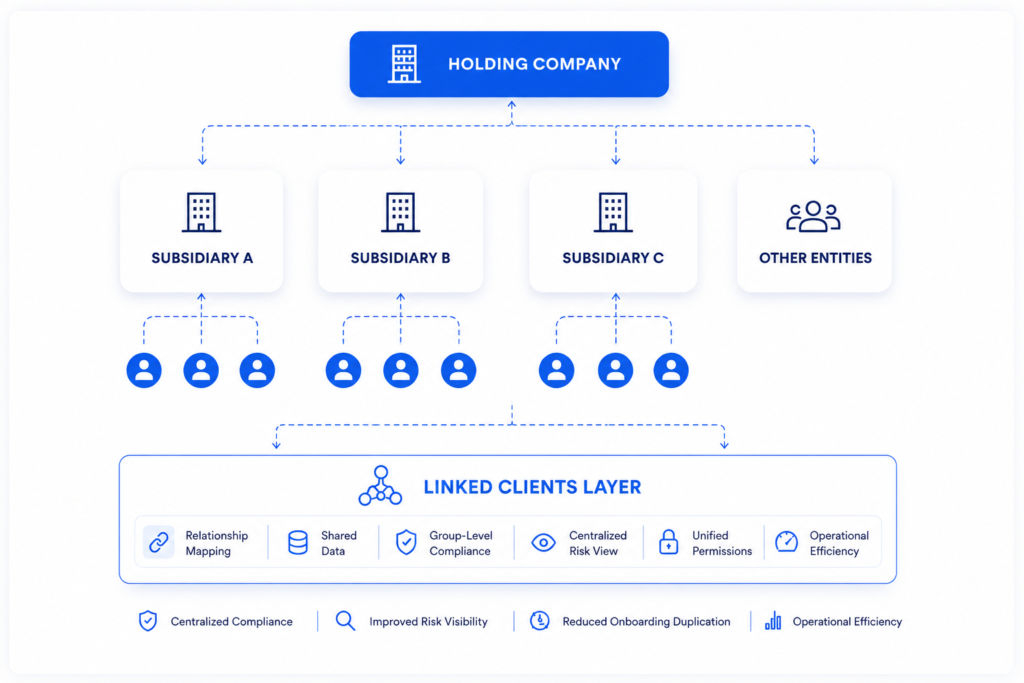

Managing Institutional Relationships at Scale

The next generation of Banking-as-a-Service platforms is moving beyond customer management and toward ecosystem management. Financial institutions are no longer serving isolated businesses. They are serving networks of connected organizations.

A modern Banking-as-a-Service provider may support a holding company, several regional entities, multiple operating subsidiaries, external partners, and hundreds of users across different jurisdictions. Understanding these relationships is critical for onboarding, compliance, risk management, permissions, reporting, and operational oversight.

This challenge has become particularly relevant for institutions operating white-label banking platforms, embedded finance ecosystems, and Banking-as-a-Service environments where a single platform may support numerous brands and organizations simultaneously.

To address this challenge, Finhost is introducing a new capability called Linked Clients.

Institutional Relationship Management with Linked Clients

Many organizations think of customer management as a collection of individual records. Linked Clients approaches the problem differently. Instead of focusing on isolated entities, it creates a relationship layer that allows institutions to understand how organizations connect to one another.

A holding company can be linked to its subsidiaries. A payment institution can visualize relationships between merchants and agents. A white-label provider can manage multiple brands through a unified framework. Compliance teams can view organizational structures rather than disconnected customer profiles.

This relationship-driven approach creates significantly greater visibility across the platform.

What Is Linked Clients?

Linked Clients is designed to help financial institutions manage complex organizational structures within a single operational environment.

Rather than onboarding and managing every legal entity independently, institutions gain the ability to understand relationships between organizations and manage those relationships more effectively. This creates a more accurate representation of how businesses actually operate.

For many institutions, the value extends beyond operational convenience. Relationship intelligence becomes a foundation for better compliance decisions, improved risk visibility, and more efficient customer management.

Why Relationship Intelligence Matters

Historically, Banking-as-a-Service platforms focused on accounts, payments, and APIs. The next phase of industry development is focused on visibility.

Financial institutions increasingly need answers to questions such as:

- Who owns this organization?

- Which entities belong to the same group?

- How are risks distributed across the structure?

- Which users should have access to which accounts?

- Which compliance reviews can be reused across connected entities?

These questions cannot be answered effectively through traditional customer records alone. Relationship intelligence provides the context required to manage complex financial ecosystems at scale.

Example Scenario

Imagine an Electronic Money Institution serving one hundred corporate customers. At first glance, this may seem manageable.

However, those one hundred customers may collectively operate hundreds of subsidiaries, branches, operational entities, and payment agents. Some may share beneficial owners. Others may operate across multiple jurisdictions. Many will have interconnected financial activity.

Without a relationship layer, compliance and operations teams must investigate these connections manually. With Linked Clients, institutions gain a centralized view of organizational structures, allowing teams to make decisions faster and with greater confidence.

Key Takeaway

Customer management is evolving. The most successful Banking-as-a-Service providers are moving beyond individual customer records and toward relationship-driven ecosystems.

As organizational structures become more complex, understanding how entities connect to one another will become just as important as processing payments or managing accounts. For institutions building Banking-as-a-Service platforms in 2026 and beyond, relationship intelligence is rapidly becoming a competitive advantage rather than an optional capability.

Compliance Is No Longer a Department. It Is Infrastructure

One of the biggest shifts in financial technology over the past decade has been the changing role of compliance. Historically, compliance operated as a separate function responsible for onboarding reviews, regulatory reporting, and occasional audits. Modern Banking-as-a-Service environments require a fundamentally different approach.

Compliance can no longer exist as an isolated department operating alongside technology and operations. This shift is also reflected in European regulation. The Digital Operational Resilience Act (DORA) requires financial institutions to strengthen ICT risk management, continuously monitor critical third-party providers, improve incident reporting, and embed operational resilience across their technology environment. As a result, compliance is increasingly becoming an architectural requirement rather than a standalone business function.

It must become part of the infrastructure itself.

Every customer interaction creates compliance obligations. Customer onboarding requires identity verification, business verification, sanctions screening, and risk assessment. Payment processing requires transaction monitoring, fraud detection, and behavioral analysis. Customer lifecycle management requires periodic reviews, document refreshes, and ongoing risk evaluation.

As customer volumes grow, manual processes quickly become unsustainable.

The most successful Banking-as-a-Service providers embed compliance directly into operational workflows. Verification processes become part of onboarding. Monitoring becomes part of payment processing. Risk scoring becomes part of customer management. Reporting becomes part of day-to-day operations rather than a separate regulatory exercise.

This approach creates significant operational advantages. Customer onboarding becomes faster, investigations become more structured, and compliance teams gain better visibility into emerging risks. Most importantly, institutions can scale without increasing operational complexity at the same pace as customer growth.

The regulatory landscape is also becoming more demanding. Frameworks such as DORA, PSD3, evolving AML requirements, and increasingly sophisticated sanctions programs require financial institutions to maintain continuous oversight across their entire ecosystem.

For this reason, modern Banking-as-a-Service architecture should be designed around the assumption that compliance touches every layer of the platform. The question is no longer whether compliance should be integrated into operations. The question is how deeply it should be embedded.

Choosing the Right Infrastructure Partners

Even the most sophisticated Banking-as-a-Service platform cannot operate entirely in isolation.

Modern financial infrastructure is increasingly built around specialized providers that deliver banking connectivity, payment processing, identity verification, compliance tooling, digital asset infrastructure, and communication services. The challenge is not selecting individual vendors. The challenge is orchestrating multiple providers within a unified operational framework.

Most institutions underestimate this complexity during the planning phase. Integrating a single provider is relatively straightforward. Managing multiple providers with different APIs, service levels, operational requirements, and regulatory obligations is significantly more challenging.

A typical Banking-as-a-Service deployment may involve banking infrastructure partners, payment providers, identity verification services, card processors, communication platforms, and digital asset infrastructure operating simultaneously.

This is one of the reasons why platform architecture matters so much. Poorly designed integrations often create operational bottlenecks, fragmented customer experiences, and unnecessary maintenance costs.

Successful Banking-as-a-Service providers focus on creating an orchestration layer that allows specialized providers to work together seamlessly. This approach creates greater flexibility and reduces dependency on any single vendor. For financial institutions operating across multiple jurisdictions, this flexibility can become a significant competitive advantage.

Build vs Buy: The Real Strategic Question

One of the most common questions facing financial institutions is whether to build a Banking-as-a-Service platform internally or adopt an existing infrastructure solution.

The discussion is often framed as a technology decision. In reality, it is primarily a business decision.

Building internally provides maximum flexibility and control. Institutions can design every workflow according to their own requirements and maintain complete ownership of the technology stack. For organizations that require long-term control without investing years in development, a source code license can provide a practical middle ground between fully custom development and traditional SaaS solutions.However, this approach also requires substantial investment in development, compliance integrations, operational tooling, infrastructure management, testing, security, and ongoing maintenance.

The challenge is not building a platform. The challenge is building an ecosystem.

Many organizations underestimate the effort required to coordinate onboarding, compliance, banking connectivity, payment infrastructure, customer management, reporting, and operational controls simultaneously.

This is why many financial institutions increasingly adopt modular infrastructure models. Rather than building every component from scratch, they focus internal resources on areas that create competitive differentiation while leveraging existing infrastructure for foundational capabilities.

The most successful organizations are often those that clearly understand which capabilities should be owned and which can be accelerated through trusted technology partners.

The Future of Banking-as-a-Service

The Banking-as-a-Service industry is entering a new phase of development. The first generation focused primarily on APIs and banking connectivity. The second generation focused on payments, accounts, and embedded finance. The next generation will focus on ecosystem management.

As financial institutions support increasingly complex organizational structures, the ability to understand relationships between customers, subsidiaries, partners, agents, and service providers becomes increasingly important. Visibility, governance, and relationship intelligence are becoming just as valuable as payment processing capabilities.

This shift is creating demand for new platform capabilities that extend beyond traditional customer management. Institutions need to understand not only who their customers are, but also how those customers are connected. This is precisely where relationship-driven infrastructure, such as Linked Clients, begins to create measurable value. The future of Banking-as-a-Service will not be defined solely by payment rails, APIs, or account structures. It will be defined by how effectively financial institutions manage increasingly complex financial ecosystems.

How Finhost Helps Financial Institutions Launch BaaS Products

To support faster implementation, Finhost offers ready-made integrations with banking, payment, compliance, and digital asset providers, allowing institutions to build solutions around their preferred infrastructure rather than starting integrations from scratch. The platform supports multiple deployment models, including SaaS and Source Code License, enabling organizations to choose the level of ownership and customization that best fits their long-term technology strategy.

Beyond the software itself, Finhost also provides implementation support, API integration services, and technical expertise to help financial institutions launch digital banking products more efficiently. This allows clients to focus on product development, regulatory readiness, and customer growth while leveraging a platform built specifically for modern financial services.

Conclusion

Banking-as-a-Service has evolved far beyond APIs, payment rails, and account infrastructure. Financial institutions launching BaaS products in 2026 must think beyond individual features and focus on building scalable ecosystems that can support onboarding, compliance, payments, operational management, and increasingly complex customer relationships.

The most successful platforms are not necessarily those with the largest number of integrations. They are the ones that combine technology, compliance, and operational processes into a unified architecture that can scale efficiently as the business grows.

As financial ecosystems become more interconnected, institutions need greater visibility into how customers, subsidiaries, partners, and agents relate to one another. Relationship intelligence is emerging as a new layer of financial infrastructure, helping organizations improve compliance oversight, reduce operational complexity, and make better decisions across their entire customer base.

For institutions evaluating their Banking-as-a-Service strategy, the challenge is no longer simply how to launch faster. The challenge is how to build a platform that remains scalable, compliant, and operationally efficient as customer structures, regulatory requirements, and market expectations continue to evolve.

The future of Banking-as-a-Service belongs to platforms that combine banking infrastructure with operational intelligence. Those that can successfully manage both will be best positioned to support the next generation of financial services.

Frequently Asked Questions

What is Banking-as-a-Service (BaaS)?

Banking-as-a-Service is a model that allows regulated financial institutions to provide banking capabilities through APIs, digital channels, or white-label platforms. These capabilities may include accounts, payments, cards, onboarding, compliance services, and other financial products.

Who uses Banking-as-a-Service platforms?

BaaS infrastructure is commonly used by banks, electronic money institutions, payment institutions, fintech companies, embedded finance providers, and organizations launching digital financial products.

How long does it take to build a Banking-as-a-Service platform?

Building a platform from scratch can take anywhere from 18 to 36 months depending on the scope, regulatory requirements, and integrations involved. Using modular or white-label infrastructure can significantly reduce implementation timelines.

What are the most important components of a modern BaaS platform?

A modern Banking-as-a-Service platform typically includes customer onboarding, compliance infrastructure, account management, payment connectivity, operational controls, reporting capabilities, and customer relationship management.

Why is institutional relationship management important?

Many financial institutions serve customers that operate through multiple legal entities, subsidiaries, partners, or agents. Understanding these relationships improves compliance oversight, risk visibility, operational efficiency, and customer management.

What is Linked Clients?

Linked Clients is an upcoming Finhost capability designed to help financial institutions manage relationships between connected organizations within a single platform environment. It provides greater visibility into ownership structures, organizational hierarchies, permissions, and risk exposure across multiple entities.