Where Should Fintech Customer Data Be Stored? A Practical Guide for UK, EU, Swiss, Canadian, and MENA Financial Institutions

July 14, 2026

Every financial institution eventually reaches the same crossroads. The business is growing. New markets are opening. Banking partners have been selected. The product roadmap is taking shape. Then a seemingly simple question emerges:

Where should we store our customer data?

At first glance, the answer appears obvious. Many founders and technology teams assume that customer information must always remain in the country where the institution is licensed or operates. In practice, however, modern financial infrastructure is far more complex.

Data residency is rarely determined by a single regulation. Instead, infrastructure decisions are shaped by a combination of regulatory expectations, cross-border data transfer rules, banking partner requirements, cybersecurity policies, operational resilience objectives, and long-term business strategy. Two financial institutions operating under the same licence may deploy completely different architectures while remaining equally compliant.

The industry itself is moving in this direction. According to Deloitte’s 2024 Banking & Capital Markets Data and Analytics Survey, 52% of banking organisations have already migrated more than half of their data to the cloud, while multi-cloud architectures are increasingly adopted to improve resilience, reduce vendor lock-in, and optimise performance.

This evolution changes the way financial institutions should think about infrastructure.

A Canadian Money Services Business expanding into Europe faces different architectural decisions than a Polish Small Payment Institution serving customers across the European Union. A digital asset platform combining fiat accounts with crypto custody introduces another layer of complexity. Meanwhile, a regulated financial institution operating in the MENA region may require source code ownership, on-premise deployment, and locally hosted identity verification services to satisfy Central Bank requirements.

These organisations are solving different business problems, operating under different regulatory frameworks, and serving different markets. Expecting all of them to follow the same data residency strategy simply no longer reflects how modern financial infrastructure is designed.

This is why the original question is, in many cases, the wrong one. Rather than asking:

Where should customer data be stored?

Financial institutions should ask:

How should our infrastructure be designed so that customer data can be stored, protected, governed, and scaled across multiple jurisdictions?

That distinction fundamentally changes the conversation.

Customer profiles, KYC documentation, transaction records, account balances, audit logs, AML data, analytics, and operational monitoring are not identical assets. They serve different business purposes, carry different regulatory obligations, and often require different deployment strategies. Likewise, modern banking platforms are no longer built around a single database in a single country. Increasingly, they separate the application layer from the data layer, distribute workloads across multiple regions, and design infrastructure around resilience, compliance, and future expansion rather than geography alone.

In this guide, we examine data residency from an architectural perspective.

Rather than focusing solely on legislation, we explore how financial institutions design infrastructure to support compliance, operational resilience, and international growth. We look at the deployment models commonly used across the United Kingdom, the European Union, Switzerland, Canada, and the MENA region, together with real implementation examples drawn from payment institutions, Money Services Businesses (MSBs), digital banking platforms, crypto businesses, and Banking-as-a-Service providers.

Because successful data residency is no longer about choosing the right country. It is about designing the right architecture.

Why Data Residency Is an Architecture Decision, Not Just a Compliance Requirement

For many fintech founders, infrastructure planning begins with regulation.

A licence has been obtained, legal requirements are being reviewed, and one of the first assumptions is often that customer data must simply be stored in the country where the institution operates. While regulations certainly influence infrastructure decisions, they rarely determine the architecture on their own.

In practice, financial institutions design data residency strategies by balancing multiple business, technical, and regulatory considerations simultaneously.

For example, a banking partner may require customer ledgers to remain within a specific jurisdiction. A cloud provider may offer better resilience and availability in another region. Internal security policies may require encryption keys to be managed separately from production databases. At the same time, the business may already be planning expansion into new markets, making future scalability just as important as current compliance.

This is why two organisations operating under the same regulatory framework can legitimately build very different infrastructure architectures.

One institution may deploy its application servers and databases within a single cloud region because its services are offered exclusively in one country. Another may separate the application layer from the data layer, storing customer information in one jurisdiction while operating application services across multiple regions. A third may choose a fully on-premise deployment to satisfy data sovereignty requirements imposed by regulators or enterprise customers.

None of these approaches is inherently more compliant than another. Their suitability depends on the organisation’s business model, regulatory obligations, operational requirements, and long-term strategy. Modern financial infrastructure is therefore designed around several interconnected factors rather than geography alone.

Regulatory expectations

Regulators expect financial institutions to maintain effective governance over customer information, ensure appropriate security controls, support supervisory access where required, and manage operational risks throughout the data lifecycle. Compliance is no longer evaluated solely by where data is stored, but also by how it is protected, accessed, monitored, and recovered.

Banking partner requirements

Infrastructure decisions are frequently influenced by commercial relationships. Banking partners, payment providers, card issuers, and correspondent banks may establish their own operational or contractual expectations regarding customer data, disaster recovery, encryption standards, or hosting environments. These requirements often shape infrastructure architecture just as much as regulation itself.

Operational resilience

Business continuity has become a strategic priority for financial institutions. Modern platforms are expected to continue operating despite infrastructure failures, cloud outages, or regional disruptions. As a result, disaster recovery, multi-region deployment, backup strategies, and infrastructure redundancy have become integral components of data residency planning rather than optional technical enhancements.

Security and cybersecurity

Protecting financial data extends well beyond selecting a hosting location. Institutions must determine where encryption keys are managed, how privileged access is controlled, how audit logs are protected, how sensitive information is segmented, and how security incidents can be detected and investigated. These architectural decisions often have a greater impact on overall security than the physical location of the servers themselves.

Business growth

Perhaps the most overlooked consideration is scalability. Infrastructure designed exclusively for today’s regulatory requirements may become a significant obstacle tomorrow. Financial institutions planning to expand into additional jurisdictions, integrate new banking partners, or launch new products benefit from architectures that can evolve without requiring a complete platform redesign.

The relationship between these considerations can be viewed as a sequence of architectural decisions rather than isolated compliance activities.

Each decision influences the next. This explains why successful financial institutions rarely begin infrastructure planning by selecting a cloud region. Instead, they start by defining their business model, understanding their regulatory environment, and designing an architecture capable of supporting both present-day compliance and future expansion.

Only then does the question of where customer data should reside become meaningful.

Not All Financial Data Has the Same Infrastructure Requirements

One of the most common misconceptions in infrastructure planning is the assumption that all financial data should be stored, protected, and managed in exactly the same way. In reality, modern financial platforms process multiple categories of information, each serving a different operational purpose and carrying different regulatory, security, and business requirements.

Customer identity documents, transaction records, account balances, audit logs, compliance data, analytics, and infrastructure monitoring all play distinct roles within the platform. Treating them as a single dataset often leads to unnecessary architectural complexity, higher operational costs, and reduced flexibility when expanding into new jurisdictions.

This distinction has become increasingly important as financial institutions adopt cloud-native architectures and distribute workloads across multiple regions. Rather than asking where “customer data” should reside, architects first determine what type of data they are dealing with and what requirements apply to that specific category. Only then can an appropriate deployment strategy be designed.

Different Data Types, Different Requirements

Although every financial institution has its own operating model, most platforms manage several common categories of data.

| Data Category | Typical Examples | Primary Considerations |

|---|---|---|

| Customer Profile Data | Names, addresses, contact information, customer identifiers | Privacy regulations, access control, regional data protection requirements |

| KYC & KYB Documentation | Passports, national IDs, proof of address, company documents, UBO information | Highly sensitive personal data, encryption, retention policies, identity verification |

| Transaction History | Payments, transfers, FX operations, card transactions | Regulatory retention, auditability, integrity, reporting |

| Account & Ledger Data | Balances, account status, internal ledger records | High availability, consistency, disaster recovery |

| Compliance Data | AML screening, sanctions checks, PEP screening, KYT alerts, case management | Regulatory reporting, investigation support, long-term retention |

| Audit Logs | Administrative actions, permission changes, system events | Tamper resistance, forensic investigations, supervisory reviews |

| Analytics & Product Metrics | User behaviour, product usage, aggregated reporting | Often suitable for anonymisation or pseudonymisation |

| Infrastructure Monitoring | Performance metrics, application logs, system health | Operational visibility, incident response, and lower sensitivity |

The table illustrates an important principle. These datasets may all belong to the same customer journey, but they do not necessarily belong in the same infrastructure layer.

For example, customer identity documents often require stronger encryption controls and stricter access policies than application logs. Transaction records typically have statutory retention requirements that differ from those applied to analytics data. Audit logs may need immutable storage to support regulatory investigations, while monitoring metrics can often be retained for much shorter periods.

Applying identical storage policies across every category usually creates unnecessary cost and operational overhead without improving compliance. Instead, modern financial institutions increasingly classify information according to its business function, regulatory obligations, and operational criticality before determining where and how it should be stored.

Data Residency Is No Longer About One Database

Another misconception is that data residency can be solved simply by choosing the right database location. Modern financial platforms rarely consist of a single database. Instead, they combine multiple services working together:

- customer identity management;

- transaction processing;

- document storage;

- compliance engines;

- audit logging;

- analytics platforms;

- monitoring and observability services;

- encrypted backup infrastructure.

Each of these components may have different deployment requirements. For example, customer records and KYC documentation may remain within a specific jurisdiction, while application services operate from another cloud region. Audit logs may be replicated to a dedicated disaster recovery environment, whereas anonymised analytics can be processed centrally to support product development across multiple markets.

This layered approach allows financial institutions to satisfy regulatory expectations without sacrificing scalability or operational efficiency. Rather than designing infrastructure around a single storage location, organisations increasingly build architectures where each data category is deployed according to its own regulatory and business requirements.

That shift represents one of the defining characteristics of modern financial infrastructure.

Key Takeaway

Successful data residency strategies begin with data classification, not cloud selection. Before choosing a hosting region, financial institutions should first understand:

- what information they collect;

- why they collect it;

- how it is used;

- which regulations apply;

- and what level of protection each category requires.

Only then can infrastructure be designed in a way that balances compliance, resilience, performance, and future growth.

How Financial Infrastructure Evolves

By now, one conclusion has probably become obvious. No deployment model fits every financial institution.

The way a platform is built depends on far more than technology. Business strategy, licensing, target markets, banking partnerships, internal capabilities, and regulatory expectations all influence the final design. Two companies offering similar financial products may arrive at completely different infrastructure decisions because they are solving different business problems.

Infrastructure rarely stays the same for long. A company launching its first product usually has one priority: bringing a reliable service to market without creating unnecessary complexity. As the business grows, that priority changes. New jurisdictions introduce new regulators, new banking partners, different payment rails, and different operational processes. Over time, the platform needs to adapt to all of them.

That evolution does not usually happen through a complete rebuild. Most financial institutions gradually redesign individual parts of the platform. Customer-facing applications may stay exactly as they are, while the data layer moves closer to a new market. A new compliance provider can be integrated without changing the payment engine. Additional payment rails may be introduced without affecting customer onboarding. Piece by piece, the platform becomes more flexible without losing continuity.

This is one of the defining characteristics of modern financial infrastructure. Instead of thinking about a banking platform as one large system, organisations increasingly build independent components that can evolve at different speeds. Customer data, payments, compliance, analytics, document storage, and operational monitoring become separate building blocks rather than tightly coupled modules.

Although every institution follows its own path, several deployment approaches appear repeatedly across the industry. They reflect different stages of business growth rather than different levels of technical sophistication. Understanding these approaches makes it easier to recognise which architecture is likely to support the next stage of a company’s development.

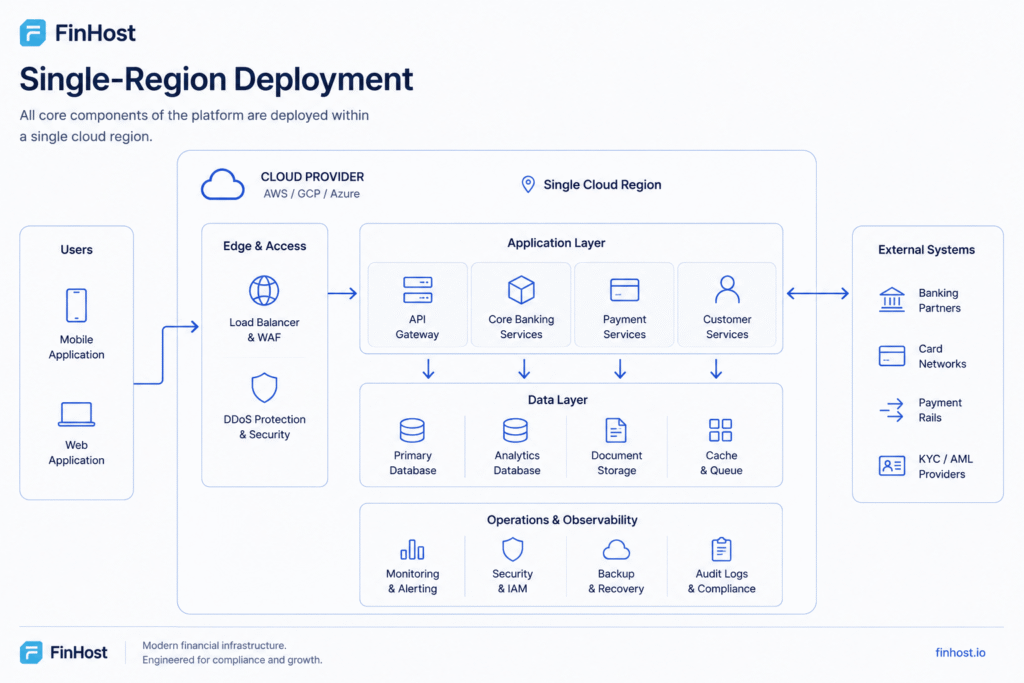

Single-Region Deployment

Most financial institutions do not begin with a globally distributed platform. In many cases, there is simply no business reason to do so. When an organisation operates under a single licence, serves customers in one jurisdiction, and works with one or two banking partners, keeping the entire platform within a single cloud region is often the most sensible decision. It reduces operational overhead, simplifies monitoring, and allows engineering teams to focus on delivering the product instead of managing infrastructure.

A simplified architecture may look as follows.

At this stage, simplicity is not a limitation. It is an advantage. Every additional component increases operational effort. Every extra region introduces new monitoring requirements, additional networking, more complex disaster recovery procedures, and higher operating costs. If the business does not yet need that complexity, adding it too early creates more problems than it solves.

Eventually, however, the business changes. The company enters another market. A second banking partner joins the platform. A local payment rail becomes necessary. Compliance requirements become more demanding. Little by little, decisions that once made perfect sense begin to constrain future growth.

This is often the moment when organisations stop asking where their servers should be located and start asking a different question. Can the application remain exactly as it is while the data moves closer to the markets where customers are served? For many growing financial institutions, the answer to that question leads to the next stage of architectural evolution.

Separating the Application Layer from the Data Layer

As financial institutions expand into new markets, one question appears surprisingly often. Does every part of the platform really need to move together? For many organisations, the answer is no.

The customer experience usually remains the same regardless of where a client opens an account. Mobile applications, web interfaces, onboarding flows, and day-to-day banking functionality are expected to work consistently across markets. The requirements behind the scenes, however, are often very different.

A banking partner may require customer records to remain within a particular jurisdiction. Another market may introduce different rules for document retention or disaster recovery. Expansion can also mean integrating new payment providers, card issuers, or identity verification services, each bringing its own operational requirements.

Rather than creating a completely separate platform for every country, many financial institutions keep a shared application layer while allowing the data layer to be deployed where it makes the most sense from both a regulatory and operational perspective.

A simplified example is shown below.

This approach allows engineering teams to continue developing a single product while giving compliance and operations teams the flexibility to meet local requirements. New markets can often be added by extending the data layer instead of rebuilding the entire platform.

One of FinHost’s recent projects illustrates this well.

A Canadian Money Services Business planned to launch a digital neobank serving customers in Canada, Europe, and the United Arab Emirates. Although the product was designed as a single banking platform, each region introduced different operational requirements. The client needed multi-currency accounts, local and international payment rails, prepaid cards, and a consistent user experience across every market. At the same time, the platform had to remain flexible enough to support future expansion without creating multiple independent systems.

Instead of developing separate platforms, the solution was built around a shared application layer with a deployment model that allowed customer data to be managed according to regional requirements. The result was a platform supporting five currencies, six payment rails, integrated foreign exchange, and prepaid Visa cards, all managed through a single operational back office. From project kickoff to production, the initial release took approximately eight weeks.

The technical implementation is described in more detail in our case study: Canadian MSB: Global Digital Neobank.

What makes this approach attractive is not simply regulatory flexibility. It also reduces the amount of duplicated infrastructure that engineering teams need to maintain. Product improvements are delivered through one application platform, while data management can evolve alongside the business as new jurisdictions are added.

For organisations with international ambitions, this often becomes the first major step away from a traditional single-region deployment.

Designing for Multiple Regions

Separating the application layer from the data layer solves one important challenge, but it does not solve every challenge. As financial institutions continue to grow, infrastructure becomes increasingly influenced by geography. New countries bring new banking partners, local payment schemes, different customer expectations, and, in some cases, entirely different regulatory frameworks.

At this stage, companies stop thinking about expansion as adding another market. Instead, they begin thinking about operating several markets simultaneously. This changes the way infrastructure is designed.

Rather than treating every region as an extension of the original platform, organisations start building regional capabilities into the platform itself. Some services remain shared because they benefit from a single implementation. Others become regional because local requirements make standardisation impractical.

The result is a platform that feels unified to customers while operating as a collection of interconnected regional services behind the scenes.

A simplified example is shown below.

One example comes from a Polish Small Payment Institution (SPI) that planned to expand payment services across more than thirty European countries.

The company already held an SPI licence and had an established customer base. The challenge was not obtaining regulatory approval but replacing operational processes that had become increasingly difficult to scale. Manual reviews, spreadsheets, and disconnected systems were creating friction for both customers and internal teams.

Instead of building separate platforms for different markets, the institution introduced a shared banking platform with regional payment capabilities. EUR and PLN services were launched first through a local banking partner, while the underlying platform was prepared to support GBP and USD as the business expanded. Mobile applications and the card programme were intentionally delivered in a second phase, allowing the company to enter the market quickly without redesigning the platform later.

Perhaps the most interesting aspect of the project was not the technology itself but the planning behind it.

Some capabilities were built because they were immediately required. Others were designed in advance because the company already knew they would become necessary as new markets were added. That approach reduced future development effort and allowed expansion without disrupting existing operations.

A more detailed description of this implementation is available in our case study, European SPI: Cross Border Payment Platform

This approach illustrates an important principle. Infrastructure should not only support the business as it exists today. It should also make the next stage of growth easier. For many financial institutions operating across Europe, that balance between present requirements and future flexibility becomes one of the defining characteristics of a successful platform.

Sometimes the Right Choice Is Not SaaS

Most fintech companies launch their products using a SaaS platform, and for many businesses that remains the right decision throughout their growth. There are situations, however, where the conversation changes completely. Some financial institutions are not looking for a managed platform. They want to own the platform itself.

The reasons vary. Local regulations may require infrastructure to remain inside the country. Internal security policies may prohibit the use of shared cloud services. In other cases, the organisation already has a large technology department and wants full control over future product development.

When these priorities become more important than deployment speed, the operating model changes as well. One recent project illustrates this particularly well.

A licensed financial institution in the MENA region approached FinHost with requirements that were fundamentally different from those of a typical SaaS customer. The organisation wanted the platform deployed inside local infrastructure, ownership of the source code, and an engineering team that could work alongside its internal developers rather than replacing them. The project involved much more than installing software.

Regional banking integrations replaced global providers. Identity verification was connected to locally approved services. Infrastructure was deployed inside local data centres, and knowledge transfer became an essential part of the implementation so that the client’s own engineers could continue developing the platform independently. In this case, data residency was only one part of the discussion.

The institution was equally concerned with operational independence, long-term ownership, and the ability to evolve the platform without relying entirely on an external vendor. For organisations operating under similar regulatory or strategic constraints, these considerations often become just as important as licensing or cloud infrastructure.

The complete implementation is described in the MENA Region: On-Premise Core Banking with Dedicated Team

Bringing Fiat and Digital Assets Together

One of the biggest changes in financial infrastructure over the past decade has been the convergence of traditional banking and digital assets. Many early crypto businesses operated alongside the banking system rather than within it. Customers often had to move between separate platforms to hold fiat balances, manage digital assets, or exchange one for the other. While this approach allowed products to launch quickly, it also introduced operational complexity and fragmented the customer experience.

That model is gradually changing. Financial institutions increasingly want to provide a single platform where customers can hold both fiat and digital assets, move between them seamlessly, and complete compliance checks through one onboarding process. A recent project demonstrates how this can be achieved.

The client was a licensed Virtual Asset Service Provider that wanted to combine traditional financial services with digital asset custody. Instead of operating separate systems, the objective was to create a single platform where customers could manage EUR, USD, and GBP accounts alongside cryptocurrency wallets, exchange between fiat and crypto, and access all services through one interface.

Achieving that goal required much more than integrating a wallet provider.

The platform combined regulated banking partners, Fireblocks custody infrastructure, a real-time exchange engine, AML controls for fiat transactions, and continuous KYT monitoring for blockchain activity. Although these services operated very differently behind the scenes, customers experienced them as a single financial product.

Perhaps the most important lesson from this project is that modern financial infrastructure is no longer defined by individual technologies. Customers do not think in terms of payment rails, custody providers, or compliance engines. They expect one coherent financial experience. Building that experience requires an infrastructure capable of bringing together multiple specialised services without exposing the underlying complexity.

The complete implementation is available in Global VASP: Crypto-Fiat Bridge Platform

Choosing the Right Deployment Strategy

After looking at several infrastructure approaches, it is natural to ask whether one of them can be considered the right choice. In practice, the answer depends far less on technology than many organisations expect.

Deployment decisions are rarely driven by cloud providers or database technologies. They usually reflect much broader business objectives. A company preparing to launch its first product is solving a different problem from a financial institution entering several new jurisdictions. Likewise, an organisation planning to build its own engineering capabilities will approach infrastructure differently from one that prefers to rely on a managed platform. This is one of the reasons why similar financial institutions often make very different technical decisions.

Two payment companies may hold comparable licences and offer almost identical products, yet adopt completely different deployment models because their long-term strategies are not the same. One may prioritise rapid market entry and operational simplicity. Another may invest in infrastructure that supports gradual international expansion. A third may consider technology itself to be a strategic asset and choose to retain full control over future development.

The projects discussed throughout this article reflect that diversity. The Canadian MSB focused on launching a multi-currency platform that could expand into several regions without duplicating the application. The European SPI designed its platform around gradual growth across the European market. The financial institution in the MENA region prioritised ownership, local infrastructure, and operational independence. The VASP project approached the challenge from another direction, bringing together traditional banking services and digital assets within a single operating environment.

Each organisation reached a different technical solution because each organisation started with a different business objective. For that reason, infrastructure planning is most effective when it begins with the business itself. Technology should support the operating model, not define it. Once the direction of the business is clear, decisions about deployment, data residency, integrations, and operational processes become considerably easier to make.

Supporting Different Infrastructure Strategies

Throughout this article, we have explored financial institutions operating under different regulatory frameworks, serving different markets, and pursuing different business goals. Despite these differences, they all faced the same underlying challenge. They needed infrastructure capable of adapting to the way their organisations were evolving.

Some required a managed platform that could be deployed quickly. Others needed regional data residency to support international operations. Some organisations preferred complete ownership of their technology, while others focused on combining traditional banking services with digital assets within a single customer experience.

These examples demonstrate that modern financial infrastructure is no longer built around a single deployment model. Flexibility has become just as important as functionality. This is the principle behind FinHost’s deployment approach.

Rather than prescribing one way to build a financial platform, FinHost supports different operating models depending on the needs of each institution. The platform can be deployed as a managed SaaS solution, configured to support regional data residency requirements, or delivered as an on-premise installation with source code licensing and dedicated engineering support. The objective is not to fit every organisation into the same architecture, but to provide a technical foundation that can evolve alongside the business.

That flexibility becomes increasingly valuable as financial institutions expand into new markets, introduce new products, or respond to changing regulatory expectations without rebuilding the entire platform.

Supporting Different Growth Strategies

Every financial institution begins with a different ambition.

Some are preparing to launch their first product. Others are expanding into new jurisdictions, replacing legacy infrastructure, or bringing together traditional financial services and digital assets. Although these organisations often operate under different licences and regulatory frameworks, they all face the same challenge sooner or later.

Technology must continue supporting the business as the business changes. That is not always easy.

Infrastructure decisions made during the first product launch often remain in place for years. If they are too rigid, every new market, banking partner, or regulatory requirement becomes another engineering project. If they are designed with flexibility in mind, growth becomes a process of extending the platform rather than rebuilding it.

This idea appears repeatedly throughout the examples discussed in this article.

The Canadian MSB was preparing for international expansion from the very beginning. The European SPI designed its platform so new markets could be added without changing its core operating model. The financial institution in the MENA region viewed technology as a long-term strategic asset and chose full ownership of its platform. The VASP project demonstrated that even services built around different financial products can operate within a unified customer experience when the underlying infrastructure is designed accordingly.

These organisations reached different technical solutions because they were solving different business problems. That is precisely the principle behind FinHost.

Rather than assuming every financial institution should adopt the same deployment model, the platform is designed to support different operating strategies. Depending on business objectives, regulatory requirements, and internal capabilities, it can be delivered as a managed SaaS solution, configured for regional data residency, or deployed on premises with source code licensing and dedicated engineering support.

The deployment model changes. The underlying principle does not. Technology should adapt to the business, not the other way around.

Conclusion

The question that opened this article was intentionally simple.

Where should customer data be stored?

After exploring different regulatory environments, deployment models, and real implementation examples, the answer is probably less straightforward than it first appeared.

There is no single country, cloud region, or infrastructure model that is universally correct. The right decision depends on the way a financial institution intends to operate, expand, and evolve over time.

For some organisations, a single-region deployment will remain the most practical choice. Others will separate the application layer from the data layer as they enter new markets. Some will build regional infrastructure across multiple jurisdictions. Others will require complete ownership of their technology through an on-premise deployment.

Each approach can be the right one when it reflects the realities of the business. Perhaps that is the most important lesson. Data residency should never be viewed as an isolated compliance exercise. It is part of a much broader conversation about resilience, operational flexibility, customer trust, and long-term growth.

Financial technology will continue to evolve. Regulatory expectations will evolve with it. Institutions that build adaptable infrastructure today will be in a much stronger position to respond to those changes tomorrow.

Ultimately, the question is not simply where customer data should reside. It is whether the platform behind it has been designed to grow with the business.