Cloud Banking as Future of Banking

September 16, 2022

Cloud computing is the next generation promising technology for the banking sector. The financial institution’s competitiveness defines the future of banking in developing and deploying banking software. The technology boosted its significance during the pandemic 2020 when cloud-native fintech companies kept their operations as smooth as ever. Moreover, it made financial institutions shake hands and partner with the world’s best cloud providers like Azure and AWS, offering long-term partnerships.

According to a survey conducted in 2021, IT executives in the banking sector chose cloud-based computing as the ideal strategy to be implemented to accelerate their progress, creating a revolution in the digital banking transformation. As a result, banking strategies have shifted to digital core and banking software adoption platforms.

Since it is one of the greatest emerging demands worldwide, this articulated piece of writing will guide you through. By the end of the article, you will be able to answer the following questions.

- How does cloud core banking work?

- Cloud is the key enabler of agile technological innovation in banking software.

- The importance of White-Label Digital Banking Platform.

- The difference between cloud-based digital banking and an on-premise banking system.

- The advantages of cloud-based digital banking.

- The emerging use of BaaS and its advantages.

- The rising competitive market of emerging cloud banking is the future.

What is cloud-based banking?

Cloud-based banking refers to managing banking infrastructure deployed on the cloud. It refers to the part where the physical servers are replaced with cloud-based technology working with cloud-based providers such as Microsoft, Google, and Azure, handling complex infrastructure by charging an amount to utilize the resources.

How does cloud core banking work?

Cloud-enabled core banking is the current age adoption of migrating their bank infrastructure over to the cloud by multiple financial institutions.

The system allows the banks to move data from one designated bank’s data center to where data can be exchanged between multiple parties after being fetched from the cloud anytime, anywhere. It happens so by APIs affect data exchange between numerous various parties.

Cloud-based digital banking vs. On-premise software

Evolving the banking sector with cloud-based digital banking has highlighted the importance of data-driven decisions and processes. So let us discuss the difference between cloud-based digital banking and how it outweighs the on-premise software.

The on-premise software has the infrastructure, high investment return, and data backup. On the contrary, using cloud-based digital banking keeps data secure, is easily deployed, and, most importantly, is budget-friendly.

On-premise software effectively syncs the tool to your company’s software applications. One great example is the implemented CRM module system, especially in the banking sector. The module in a CRM is integrated with the respective modules present in the database system to ensure a smooth and proper flow of banking processes.

On the contrary, cloud-based digital banking allows bank professionals to access information from any bank and any part of the world. Cloud-based banking software is hosted off-site by the provider and does not bind the user to access data from physical servers only.

On-premise vs Cloud-based

| Feature | On-premise | Cloud-based |

|---|---|---|

| Security | Organization’s responsibility | Service provider responsibility |

| Customization | Difficult | Simple |

| Updates | Organization has choice | No choice |

| Ownership | Complete ownership of server and data | Only data ownership |

| Audit | Difficult | Simple |

| Connectivity | Might be difficult after working hours | Data access from anywhere anytime |

| Affordability | Only big size organization | All size organization |

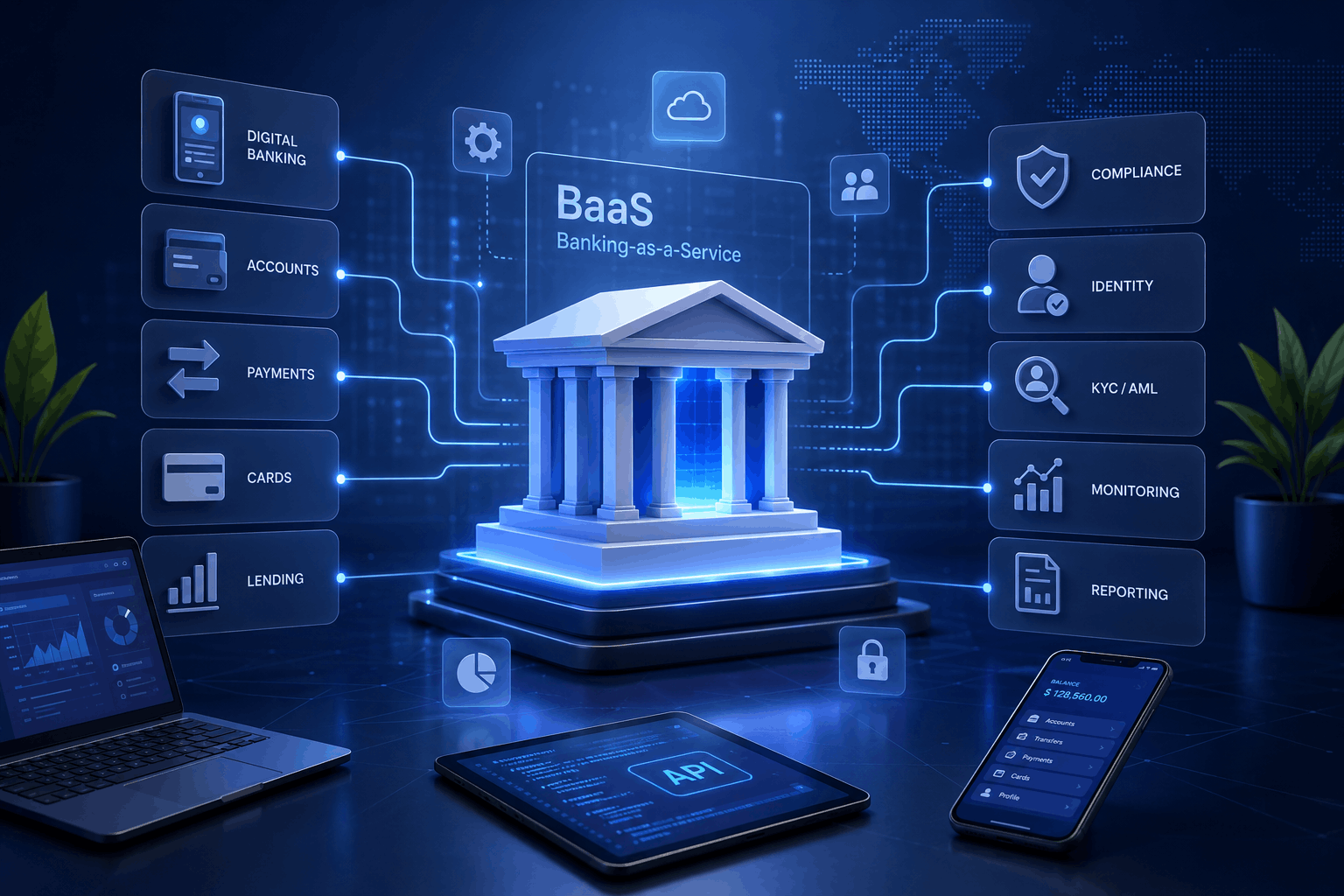

White-Label digital banking platform for Banking in the Cloud

White-label banking is an example of a private-label financial service referred to as banking-as-a-service (BaaS).

Before diving deep into the explanation of white label banking, this private labeling strategy allows third-party manufacturers to produce products and sell them under the retailer’s name. In this way, the wholesale control of the brand and packaging and pricing are all in the retailer’s control, promoting customer recognition and loyalty to the brand.

Similarly, white label banking is a form of private label banking where banks provide access to their application program interfaces (API) and allow third parties to produce financial products with the bank’s existing developed infrastructure. It is a strategy that accelerates the builder’s go-to-market strategy by removing hurdles, which could be regulatory, legal, or even technical.

White Label Banking Services

When banking sectors or institutions provide a means for third-party manufacturers to develop their products, the company-branded front end is promoted under the bank’s name, with the bank’s respective compliance and technology measures.

Some of the white-label banking services include:

- Bill payment applications

- Personal Loans

- Balance statements/notifications

- Mortgages

- Debit and credit cards

- Current accounts

- Saving accounts and insurance

The future of white-label banking applications is massive. Digital technologies are creating a spark of thriving competition in the banking sector, and with white-label banking, the unrestricted banking movement is embraced everywhere.

BaaS technology is redefining the banks’ purpose and the services they are always entitled to provide. Staying ahead of the curve, the competitive markets have embraced BaaS as a trend. For example, some of the world’s largest banks in the United Kingdom encourage newcomers by investing in white-label banking services. According to inside intelligence, this will lead to more profitable ventures and encourage profitable partnerships.

Hite label banking services are one of the advantages of cloud-based digital banking, and more are discussed in the next section below.

Read more: Top Core Banking Software Companies List in 2023

Advantages of Cloud-Based Banking

Cloud-based banking has multiple advantages, from the scalability of the banking sector to its unique diversified aspects discussed in the points step by step.

Affordability

When considering traditional on-premise software has data hosted on physical servers. However, banks will not have to pay for unnecessary server costs with cloud-based digital banking. In addition, the cloud server is made to handle vendor maintenance services and enables you to use these services easily.

All the banks or financial institutions will have to do is pay the subscription fee to store all your confidential information on the cloud and access it from there.

Another interesting feature of cloud-based banking applications is that it uses a pay-per-use model, making it cost-efficient for banks to store their data and pay for the service just as they like. Furthermore, it makes it easy for all banks of all sizes to use the pay-per-use model, making it affordable.

Compatibility

Banks or financial institutions do not need to worry about the compatibility of accessing data from cloud-based digital applications. The accessibility can be done anytime and is made to facilitate any accessibility. This makes cloud infrastructure compatible enough to avoid any hassle of accessing information otherwise.

Only banks operating on legacy infrastructure might find it hard to access information while modernizing their infrastructure.

Convenience

Most banks are moving to cloud-based financial arrangements since they are helpful. Simultaneously, CSPs currently give information to the executive administrations to oversee complex cycles inside the bank.

Popularity

Amazon, Microsoft, Google, Alibaba, and Huawei rule over 80% of cloud banking sectors. These companies have massive shares in the banking market, with Amazon generating a revenue of 26,201, occupying 40.8% market share.

Fraud Detection

Monetary establishments can’t endure any information thefts; your association needs protected data management systems to shield delicate data from lawbreakers.

With cloud-based financial software, you can safeguard your computerized retail bank from vindictive outsider access. In addition, cloud-based banking applications can assist advanced economic foundations with identifying inconsistencies like fraud detection and tax evasion activities.

Analytics

Since cloud vendors offer financial arrangements with data management frameworks, banks can appreciate computerized information detailing and examination.

Environmentally Friendly

Overseeing banking tasks requires critical registering power, which influences the climate adversely. However, with distributed computing, you can keep an eco-accommodating framework for your inside and outer administrations.

SaaS Neobank Platform

This particular platform is a hybrid cloud delivery model with easy regulatory compliance, providing the possibility of switching to a source code version anytime.

Challenges of Cloud-Based Banking

Regardless of the commitments of cloud-based digital banking applications, the difficulties of this model are colossal.

Regulations

Banks and other monetary organizations should submit to different neighborhood and worldwide administrative rules concerning information sharing and utilization. Simultaneously, cloud sellers offer an alternate arrangement of consistency rules, which struggle with laid-out monetary guidelines.

Accordingly, banks should employ experts to cross-reference these clashing guidelines to keep away from fines.

Security

Despite impermeable security and protection commitments, the cloud isn’t a safe house for delicate client and company information.

Organizations like Google are scandalous for selling client information, which conflicts with GDPR consistency principles. Moreover, although the organization professes to safeguard banking information, no guarantees exist to keep their promise.

Data Migration

Moving the whole design is an earth shattering errand that most organizations battle to deal with. Truth be told, Bloor Research did a review that showed that 38% of all information relocation endeavors end in a sheer debacle.

On the off chance that your association is moving from out-of-date heritage programming, finding qualified distributed computing specialists turns into a threatening cerebral pain.

Plus, relocating cloud-based financial administrations can require a while, contingent upon the bank’s size and fundamental framework. Also, in possession of clumsy relocation experts, the cycle can upset financial activities essentially.

Outsourcing Risks

If a bank doesn’t have an appropriately prepared IT division to carry out the cloud-based financial center, it must reevaluate the relocations, which presents extra security chances.

Rethinking implies that the bank surrenders the reins of the whole financial engineering to an outsider. Like this, the bank or monetary foundations jeopardize their clients’ information.

Human Errors

Although most current cloud banks depend on computerized calculations, people compose the code and gather the center framework.

Sky News reports that “messy coding” presents more than 1 million shortcomings in the product framework that programmers can take advantage of.

Moreover, a buggy code piece can disintegrate the whole cloud foundation while making a neobank platform.

Along these lines, you can never enact human ineptitude and what it will mean for your bank’s tasks.

Unforeseen Circumstances

Aside from human mistakes, unexpected conditions can pulverize your cloud-based financial arrangements.

Server personal times and cyberattacks can render the application unusable. Also, since you have zero power over the merchant’s framework, your association will stay in an in-between state until they fix the issue.

How Can We Help You?

We at FinHost believe in enabling financial businesses to grow fast, providing ready-made integrations with multiple finance providers. Our products include digital core banking software, an in-product CRM, powerful analytics, and flexible fees and limits.

Another product is the white-label mobile digital wallet with multi-currency/multi-asset support, instant P2P transfers, and extensive integration capabilities. For more information, visit us at finhost.io and drop a query. Our team will reach out and facilitate your needs.

When you contact us, our team will reach out to you and discuss each module you need in your system. Then, it will be addressed with the project manager, who will help envision your vision and bring it to life. The project will then be initialized and created, choosing the best features to be integrated into forming your program’s modules.

The final step will be to release your project, and then the project will be yours.

FAQ’s

What is better- cloud-based digital banking or on-premise software application?

Cloud-based digital banking software is better than an on-premise application as its advantages outweigh the disadvantages. It allows the user to successfully access software applications worldwide, making the cloud-based solution more compatible and easy to use.

What are the risks of cloud-based core banking?

With cloud-based systems, information can be accessed from anywhere. Hence, this makes cloud-based banking applications prone to risks and cyber-attacks. More third-party hard-party services banks also risk control over their operational and procedural systems. Security and privacy concerns are also raised when white-label banking comes into the picture.

What kind of cloud do banks use?

Banks usually use IaaS, which means they use all relevant resources on an outsourced model.

How do banks use cloud computing?

Cloud Computing is utilized in banks for different purposes, including Customer Relationship Management (CRM): Banks use cloud-based CRM frameworks to oversee client information and associations. This permits monetary foundations to monitor all client associations, paying little mind to the area or season of day.