The Monetary Authority of Singapore (MAS): A Fintech Licensing Guide

June 5, 2026

Singapore has built a reputation as one of the world’s most sophisticated financial centers. For payment institutions, fintech startups, crypto businesses, remittance providers, and digital banking companies, the country offers something many jurisdictions struggle to balance: strong regulation combined with support for innovation.

At the center of this ecosystem stands the Monetary Authority of Singapore, commonly known as MAS. While many businesses initially view MAS simply as a regulator, its role extends much further. It shapes financial policy, develops regulatory frameworks, promotes innovation, and influences how financial infrastructure evolves across the region.

For companies considering expansion into Asia, understanding MAS is not only a compliance exercise. It directly affects licensing strategy, operational costs, launch timelines, infrastructure decisions, and future scalability.

Why Singapore Became a Strategic Market for Financial Businesses

Singapore’s position in global finance was not built solely on favorable regulation. The country created an ecosystem where regulatory credibility, international connectivity, and technology infrastructure work together.

For financial companies, Singapore provides access to Asian markets while maintaining a regulatory environment recognized by banks, institutional investors, and international partners. This matters because obtaining licenses is only one part of expansion. Establishing trusted banking relationships, onboarding clients, and entering new markets often depends on regulatory reputation.

Many payment providers, wallet businesses, digital banks, and crypto companies choose Singapore because it creates opportunities to scale regionally while operating from a jurisdiction with strong international recognition.

Companies expanding into Singapore often pursue objectives such as:

- Access to Southeast Asian markets

- Higher credibility with institutional partners

- Improved banking access

- Expansion opportunities across multiple jurisdictions

- Stronger investor confidence

These advantages explain why Singapore continues to attract both startups and established financial institutions.

What Is the Monetary Authority of Singapore and Why Does It Matter?

MAS serves several roles simultaneously. It functions as Singapore’s central bank, supervises financial institutions, regulates payment systems, and develops a long-term financial sector strategy. Unlike regulators that primarily focus on enforcement, MAS has historically taken a more ecosystem-oriented approach. It actively supports innovation programs, encourages financial technology adoption, and continuously adapts regulation to emerging business models.

This approach has become particularly important for businesses operating in sectors where regulation changes rapidly, including digital assets, embedded finance, digital banking, and cross-border payments.

For businesses entering Singapore, MAS influences nearly every operational layer, including licensing requirements, transaction monitoring expectations, technology standards, outsourcing requirements, and ongoing reporting obligations. Understanding these requirements early significantly reduces delays later in the expansion process.

How MAS Structures Financial Regulation

One of the reasons Singapore remains attractive for financial companies is the relatively structured approach to regulation. Instead of applying a single framework to all businesses, MAS generally regulates activities based on business models and financial services provided.

A company providing international transfers faces different obligations than a digital bank. A crypto platform operates under different expectations than a payment processor. This activity-based approach gives businesses flexibility, but it also creates complexity because many companies operate multiple services simultaneously.

In practice, businesses entering Singapore often evaluate four areas before choosing their regulatory pathway:

- The financial services being offered

- Target customer segments

- Geographic markets served

- Expected transaction volumes

Mistakes during this stage often lead to expensive restructuring later.

The Payment Services Act Changed How Fintech Companies Enter Singapore

One of the most important regulatory developments for modern financial businesses was the introduction of the Payment Services Act. The framework moved Singapore toward a more modular approach where licensing obligations depend on business activities rather than traditional institution categories. This shift significantly impacted payment companies, crypto businesses, remittance providers, wallet operators, and fintech platforms.

Today, businesses frequently operate under categories such as Standard Payment Institution or Major Payment Institution depending on scale and services provided. For founders, the important takeaway is that licensing decisions now directly influence infrastructure requirements, transaction monitoring obligations, compliance costs, and growth capacity. Choosing the wrong structure may create operational bottlenecks long before customer acquisition becomes a challenge.

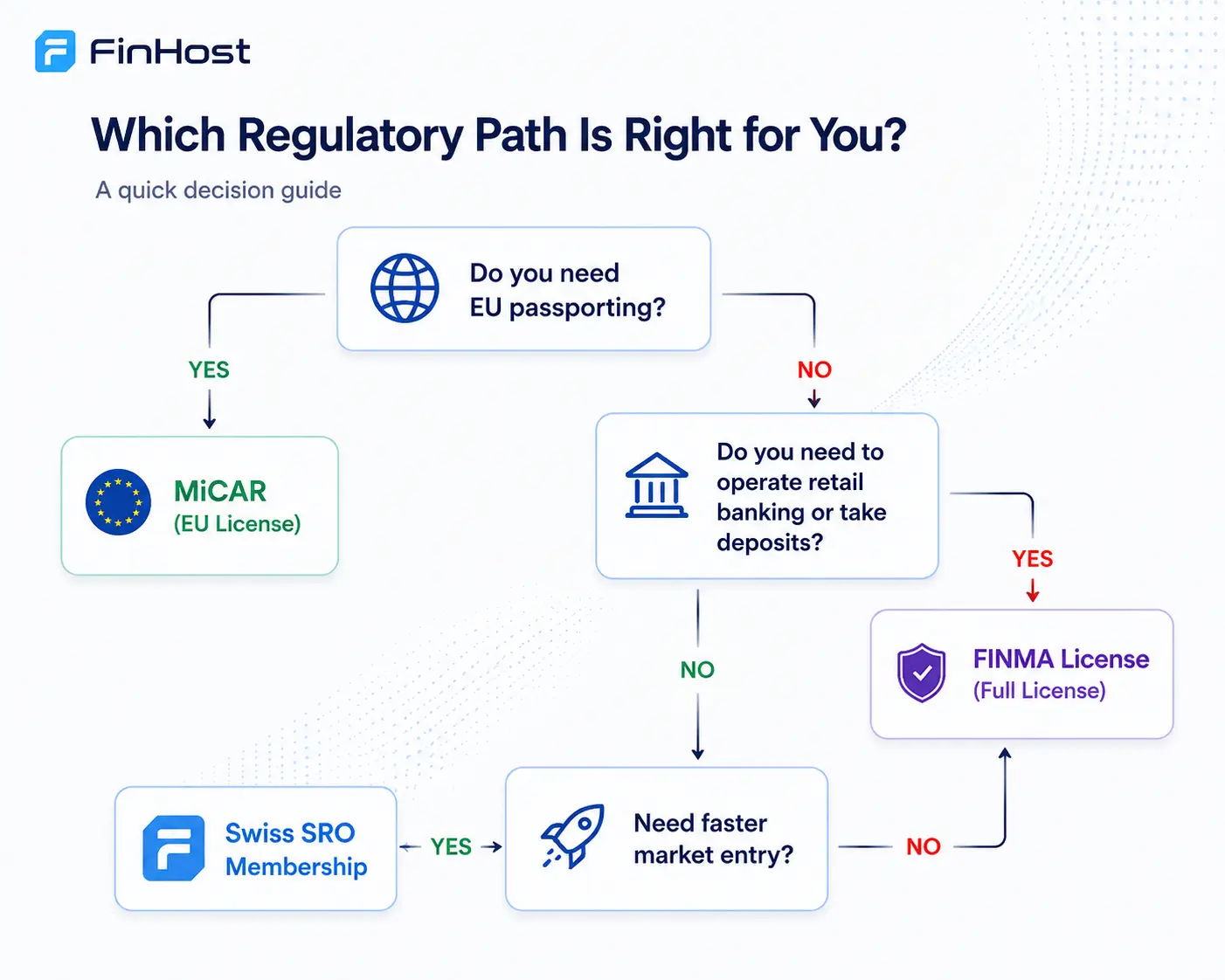

Key Licensing Pathways Under MAS

Selecting the correct regulatory path is one of the most important decisions companies make before entering Singapore. Licensing determines not only what services can be offered but also affects operational structure, compliance workload, banking relationships, and scaling opportunities. Businesses entering the market frequently evaluate several licensing routes depending on their activities.

Major Payment Institution License

The Major Payment Institution framework is commonly considered by businesses expecting larger transaction volumes or planning rapid expansion. This route is often used by payment providers, remittance businesses, wallet operators, cross-border platforms, and companies processing significant payment flows. The advantage of this structure is scalability. The tradeoff is that compliance expectations, governance requirements, and operational obligations become more demanding.

Standard Payment Institution License

This model is typically more suitable for businesses operating with lower transaction volumes or testing market opportunities before scaling. Many early-stage fintech businesses initially explore this route because it may reduce operational complexity during early growth stages. However, companies expecting rapid growth should carefully assess future transaction thresholds to avoid restructuring later.

Digital Payment Token Regulation

Singapore has developed one of the more structured regulatory approaches toward digital assets. Crypto businesses, exchanges, wallet providers, and digital asset platforms often fall within Digital Payment Token-related requirements. The regulatory environment remains supportive of innovation, but expectations around governance, risk management, customer protection, and transaction monitoring continue increasing.

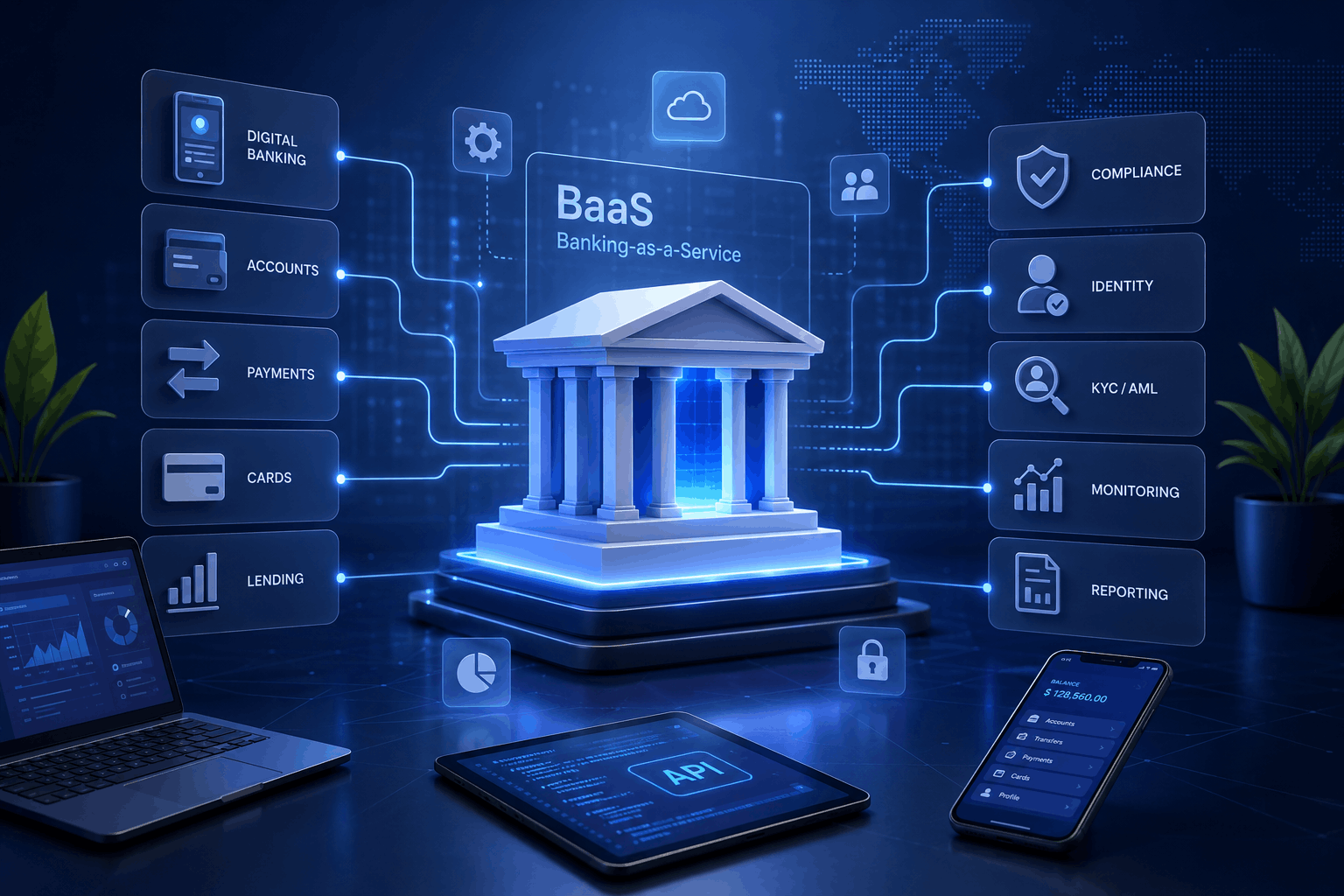

Banking and Digital Banking Frameworks

Companies building banking products, embedded finance solutions, or broader financial ecosystems may also evaluate banking-related licensing pathways. These structures generally involve significantly higher complexity levels, stronger capital expectations, and longer preparation periods. For many businesses, partnering with infrastructure providers becomes more efficient than building every operational layer internally.

Compliance Expectations Extend Far Beyond AML

Many companies entering Singapore underestimate how much compliance extends beyond customer verification. AML controls remain critical, but regulators increasingly focus on operational resilience, technology governance, cybersecurity, outsourcing risks, and internal controls. Businesses are generally expected to demonstrate clear ownership structures, documented procedures, effective governance frameworks, and ongoing monitoring capabilities.

Technology infrastructure has also become a regulatory topic. Companies increasingly need to demonstrate how systems are secured, how incidents are managed, and how operational disruptions are controlled. This creates a practical challenge for growing businesses. Expansion requires not only licensing budgets but also investments in infrastructure, compliance teams, monitoring systems, and reporting processes.

Common Challenges Companies Face When Entering Singapore

The largest market entry risks rarely come from regulation itself. Most delays appear during implementation. Companies frequently underestimate how long internal preparation takes. Licensing projects often become slower because governance structures are incomplete, operational procedures are undocumented, or technical architecture is not fully aligned with regulatory expectations.

Another challenge comes from banking relationships. Many businesses secure licensing strategies before understanding how operational banking, payment connectivity, safeguarding arrangements, or treasury operations will function. Cross-border companies also face complexity when serving multiple jurisdictions simultaneously. Singapore licensing may solve one part of expansion while creating additional obligations elsewhere.

This is why experienced operators increasingly approach market entry as an infrastructure project rather than only a licensing project.

Infrastructure Strategy Often Determines Launch Speed

Obtaining approval is only one stage of building financial products. Infrastructure decisions frequently determine how quickly businesses launch, expand, and adapt to changing regulations. Many financial companies now combine licensing strategies with pre-built technology, embedded compliance layers, payment integrations, and modular architecture.

Using a scalable approach allows businesses to focus internal resources on growth rather than rebuilding operational foundations repeatedly. Companies exploring expansion frequently evaluate solutions such as Finhost for access to modular white-label fintech infrastructure, faster deployment models, and operational frameworks designed for regulated businesses.

Businesses launching banking products increasingly prioritize white-label digital banking platform architectures because infrastructure flexibility directly affects expansion speed, integration capacity, and future product development.

For crypto-focused businesses, infrastructure selection is equally important, as transaction monitoring, wallet architecture, custody models, and compliance tooling significantly influence operational complexity.

Singapore Compared With Other Financial Jurisdictions

Singapore remains highly attractive, but it is not universally the right choice.

| Factor | Singapore | UK | EU | UAE |

| Regulatory Reputation | Very High | Very High | High | Growing |

| APAC Market Access | Excellent | Limited | Moderate | Strong |

| Crypto Framework Maturity | High | High | Developing | High |

| Licensing Complexity | Medium to High | High | Medium | Medium |

| International Recognition | Very Strong | Very Strong | Strong | Growing |

The right jurisdiction depends less on popularity and more on business model, target geography, risk appetite, and operational capabilities.

Is MAS Still the Right Choice for Financial Businesses in 2026?

Singapore remains one of the strongest jurisdictions for companies building payment products, cross-border financial services, digital asset businesses, and modern financial infrastructure. However, success in Singapore increasingly depends on preparation quality. Companies that treat licensing as a standalone project often discover unexpected operational complexity later.

Businesses that combine regulatory planning, infrastructure strategy, compliance design, and scalability considerations early usually move faster and operate more efficiently. For founders, payment companies, fintech operators, and regulated businesses, the real question is often not whether Singapore is attractive. The more important question is whether the business is operationally prepared to enter one of the world’s most sophisticated financial ecosystems.