Card Issuing: Architecture, Risk and Scale in Modern Fintech

February 26, 2026

Card issuing is often described as a product capability — a way to “add cards” to a fintech application.

In reality, card issuing is infrastructure.

Behind every debit card, crypto-linked card or embedded finance program stands a layered architecture of regulated banks, issuing processors, card networks and real-time risk engines. The structural decisions made at the beginning of a card program determine how it scales, how it withstands fraud pressure and how it performs under regulatory scrutiny.

For fintech founders, CTOs and product leaders, understanding how card issuing works is not about learning terminology. It is about understanding structural control.

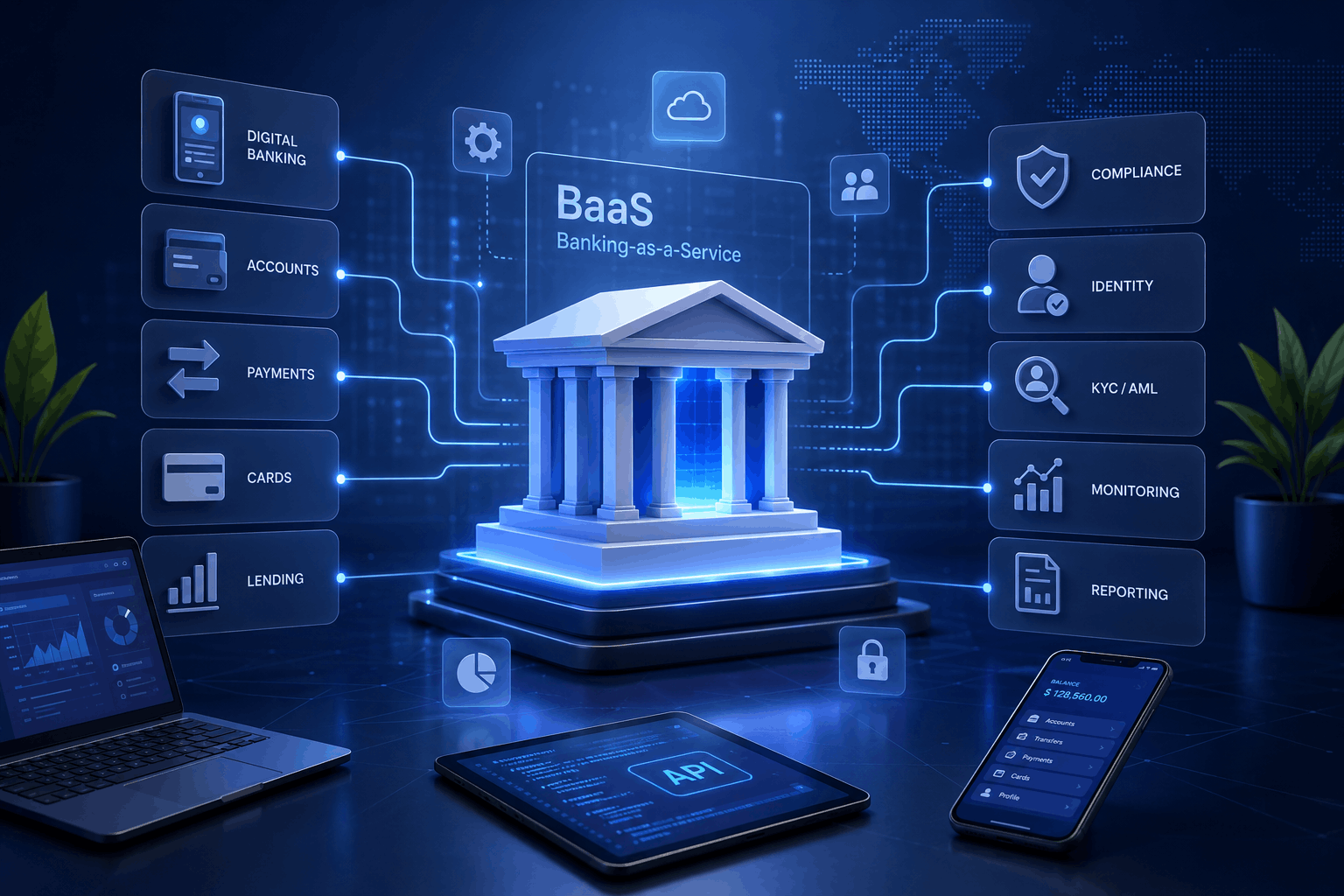

The Architecture Behind Modern Card Issing

Card issuing operates across two interconnected dimensions:

- Ecosystem structure (who is involved)

- Transaction lifecycle (how money moves)

Before diving into authorization flows, it is important to separate user experience from regulated infrastructure.

Below is a simplified architectural model illustrating both dimensions.

Card Issuing Ecosystem & Transaction Flow

The upper layer represents the structural ecosystem.

At the top sits the fintech application — the interface managing customer balances, notifications and spending controls. However, the application does not directly issue the card. It orchestrates infrastructure.

Between the user interface and the regulated entity sits a program management and API orchestration layer. This component connects onboarding flows, KYC integrations, card lifecycle logic and reporting systems.

Below it operates the issuing processor — the real-time authorization engine. This is where transaction decisions are made in milliseconds.

The regulated core of the ecosystem is the issuing bank or BIN sponsor. This entity holds the Bank Identification Number and assumes regulatory accountability for safeguarding, reporting and network compliance.

Finally, global card networks such as Visa and Mastercard route transactions, define interchange frameworks and govern clearing and settlement processes.

Most teams understand the frontend.

Fewer model the dependencies underneath.

The Transaction Lifecycle: What Happens After the Tap

When a customer initiates a payment, the process unfolds across three distinct stages.

Authorization

The merchant’s acquirer routes the request through the card network to the issuing processor. The processor evaluates balance availability, fraud rules, velocity controls and compliance flags before returning an approval or decline — typically within 200–500 milliseconds.

Latency at this stage directly affects user trust.

Clearing

Clearing usually occurs in batch format. Interchange is calculated, transaction details are finalized and network reporting is generated.

Revenue logic is defined here.

Settlement

Settlement involves net fund transfers between issuing and acquiring institutions. Treasury exposure, liquidity management and reconciliation processes operate at this stage.

Settlement timing determines capital efficiency.

Authorization defines user experience.

Clearing defines economics.

Settlement defines liquidity.

BIN Sponsorship and Licensing Strategy

Most fintech companies rely on BIN sponsorship rather than holding a direct banking license.

Under a BIN sponsorship model, a regulated bank provides the BIN and maintains regulatory oversight, while the fintech controls product logic and customer interface.

This structure accelerates market entry but introduces dependency. Fraud ratios, chargeback performance and AML compliance remain subject to network-level thresholds and sponsor oversight.

Strategic considerations include:

- control over program governance

- cross-border expansion limits

- margin structure

- regulatory exposure

For fintechs expanding into broader financial ecosystems, issuing often integrates within a white label neo bank platform environment. Crypto-enabled products may incorporate issuing into a white label crypto app stack, bridging digital asset balances with traditional card rails.

In both cases, issuing becomes part of a licensed and orchestrated financial framework rather than a standalone module.

The Risk Surface of Card Issuing

Issuing risk does not appear at launch. It appears at scale. Fraud monitoring thresholds are defined at program level. Chargeback ratios are continuously measured against network tolerances. Interchange margins fluctuate across geographies and merchant categories.

As transaction volumes increase:

- fraud vectors diversify

- monitoring complexity rises

- reconciliation becomes operationally sensitive

- sponsor-level scrutiny intensifies

Issuing therefore operates as a controlled risk environment. Infrastructure maturity determines how well a program absorbs volatility.

The Issuing Maturity Model

To better understand where a fintech stands structurally, consider the following maturity framework.

Level 1 – Feature-Based Issuing

Cards are launched primarily as a product enhancement. Infrastructure is vendor-driven. Regulatory exposure is partially understood. Fraud management is reactive.

Risk: high dependency, limited scalability.

Level 2 – Structured Integration

Processor relationships are clearer. BIN sponsorship agreements are formalized. Reporting processes exist. Fraud monitoring improves.

Risk: operational exposure remains concentrated in external partners.

Level 3 – Infrastructure Awareness

The fintech understands ledger logic, settlement timing and fraud ratios. Program governance is actively monitored. Treasury implications are modeled.

Risk: reduced but still dependent on sponsor alignment.

Level 4 – Strategic Issuing Architecture

Issuing is treated as infrastructure. Regulatory exposure is mapped. Liquidity cycles are optimized. Multi-processor redundancy may exist. Cross-border structuring is deliberate.

At this stage, issuing becomes an asset rather than a risk.

This maturity perspective reframes issuing from “integration” to “infrastructure control.”

Crypto-Linked and Embedded Issuing

Crypto-linked card programs introduce additional structural complexity.

Although the user experience suggests seamless crypto spending, backend architecture typically includes real-time asset conversion, fiat settlement and AML monitoring across both blockchain and traditional payment systems.

Embedded finance introduces similar dynamics. Marketplaces and SaaS platforms embed issuing to extend financial services into their ecosystems.

In both scenarios, issuing acts as a liquidity extension layer — not merely a payment instrument.

Issuing as a Structural Decision

Card issuing is easy to integrate. It is difficult to operate responsibly at scale.

For modern fintech platforms, issuing determines liquidity structure, revenue mechanics and regulatory positioning. It is not a feature layered onto a product — it is the infrastructure enabling financial interaction.

Treating issuing as architecture rather than integration is what separates scalable platforms from fragile ones.

Issuing as a Structural Decision

Card issuing is easy to integrate.

It is difficult to operate responsibly at scale.

For modern fintech platforms, issuing determines liquidity structure, revenue mechanics and regulatory positioning. It is not a feature layered onto a product — it is the infrastructure enabling financial interaction.

Treating issuing as architecture rather than integration is what separates scalable platforms from fragile ones.

Strategic Considerations Before Launch

Before deploying a card program, enterprise fintech teams should clarify four structural questions:

- Who controls ledger reconciliation?

- Who absorbs fraud volatility?

- Who manages regulatory reporting?

- Who governs settlement liquidity?

The answers define scalability.

Infrastructure orchestration approaches — including licensed, modular frameworks available via Finhost — allow fintech teams to align issuing architecture with long-term regulatory and operational strategy.

Launching quickly is valuable. Launching sustainably is critical.

FAQ: Card Issuing in Modern Fintech

What is card issuing in fintech?

Card issuing refers to the regulated process of providing debit, credit or prepaid cards to customers, supported by an issuing bank or BIN sponsor and connected to global card networks for transaction processing.

How does BIN sponsorship work?

BIN sponsorship allows a fintech to operate a card program under a licensed bank’s regulatory umbrella. The sponsor provides the BIN and assumes regulatory oversight, while the fintech manages customer experience and product logic.

What is the difference between a card issuer and a card network?

A card issuer (typically a bank or regulated entity) issues cards and manages customer accounts. Card networks such as Visa and Mastercard route transactions and govern clearing and settlement infrastructure.

Is card issuing profitable for fintech companies?

Profitability depends on scale, interchange rates, fraud performance, operational costs and licensing structure. Issuing can become profitable at scale, but requires disciplined risk management and treasury oversight.