What Is Digital Banking in 2026? The Structural Evolution of Financial Infrastructure

February 18, 2026

Digital Banking Infrastructure in 2026: From Mobile Apps to Regulated Financial Architecture

For years, digital banking was synonymous with interface innovation. The winners were those who removed friction from onboarding, reduced fees, and optimized mobile journeys. But by 2026, the definition has shifted fundamentally.

Digital banking is no longer a distribution model. It is a regulated financial infrastructure operating within defined capital requirements, operational resilience frameworks, and increasingly AI-dependent architectures.

McKinsey’s Global Banking Annual Review 2025 shows that banks generated $5.5 trillion in revenues after risk cost in 2024, pushing net income to a record $1.2 trillion. Yet the industry’s valuation lags other sectors by nearly 70%. The explanation is structural: markets expect margin compression, AI-driven disruption, deposit competition, and increasing regulatory intensity.

In this environment, digital banking cannot be defined by UX. It must be defined by architecture.

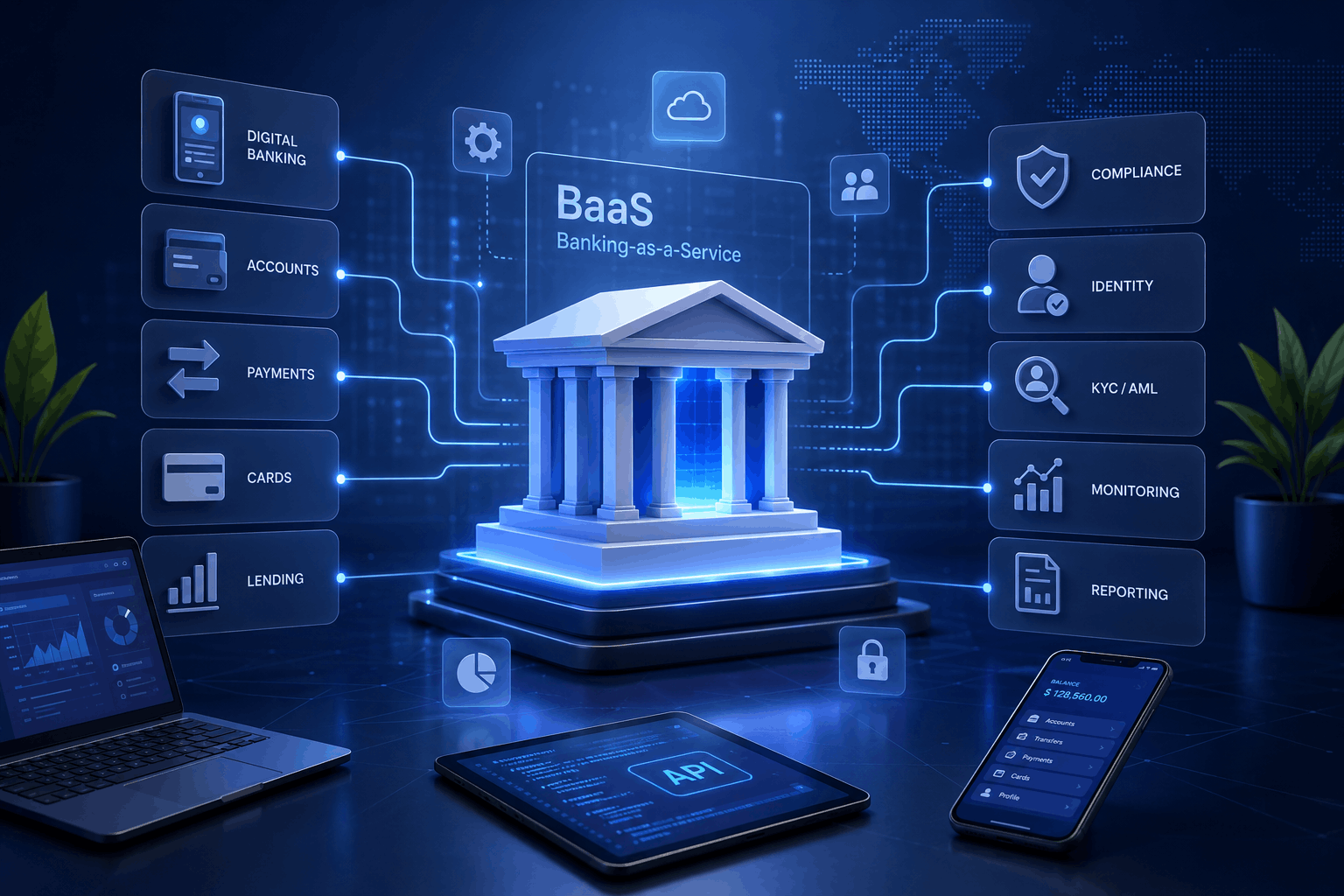

For new entrants, this often means launching within a unified environment such as a white label digital bank infrastructure, where regulatory alignment, core banking, compliance automation, and payment rails are pre-integrated into a single operational model.

The Structural Layers of Digital Banking Infrastructu

Digital banking in 2026 operates across multiple interdependent layers, but unlike earlier years, these layers are no longer modular add-ons. They form a single regulated system.

The structural architecture of digital banking in 2026 can be visualized as an integrated infrastructure stack:

At the base of this architecture sits the regulatory perimeter. Licensing structure, capital adequacy, liquidity buffers, supervisory reporting, and board-level governance define the boundaries within which the institution is allowed to operate.

Deloitte’s 2026 outlook notes that US banks maintain CET1 ratios above 14%, yet margin compression and macro uncertainty mean that capital strength alone is insufficient. Precision in capital deployment has become a strategic necessity.

Resting on this regulatory foundation is the core banking engine — the ledger architecture that governs accounts, reconciliation logic, liquidity positioning, and product configuration. In 2026, failure at this level is no longer a technical inconvenience. It is a supervisory exposure, often accompanied by regulatory scrutiny and reputational risk.

Compliance automation forms the next critical layer. The filing of 2.6 million Suspicious Activity Reports in the United States during 2024 illustrates the scale at which financial crime monitoring now operates. AML, KYC, sanctions screening, and real-time transaction analysis are not auxiliary systems; they are embedded control mechanisms woven directly into transaction flows.

Payments infrastructure extends this architecture outward. What once consisted primarily of SEPA, SWIFT, and card networks now increasingly includes instant settlement mechanisms, tokenized assets, and programmable rails. At this intersection, digital banking begins to converge with digital asset infrastructure, reshaping liquidity velocity and settlement design.

Distribution occurs at the customer and API layer — through mobile interfaces, web platforms, and embedded integrations. Increasingly, institutions rely on unified environments such as a white label neo bank platform to ensure that compliance, core banking, and digital experience are not developed in isolation but orchestrated within a coherent system.

Yet across all layers, one element proves decisive: data maturity. Deloitte repeatedly emphasizes that fragmented and poorly governed data environments undermine AI scalability. Without reliable lineage, interoperability, and governance controls, even sophisticated models fail to produce durable value.

Digital banking in 2026 is therefore not simply a stack of technologies. It is a synchronized system in which regulatory discipline, core infrastructure, compliance automation, programmable payments, and AI-ready data operate as a single institutional architecture.

AI in Digital Banking 2026: Productivity Engine or Profit Disruptor?

AI is often discussed as a productivity tool, but in 2026 it is a structural variable.

McKinsey estimates that AI could generate gross cost reductions of up to 70% in selected categories, translating into a net cost-base reduction of roughly 15–20% after accounting for increased technology spending. For banks under margin pressure, this is significant.

Yet AI simultaneously threatens core profit pools.

Agentic AI systems capable of autonomously optimizing deposits and credit decisions may reduce customer inertia. McKinsey estimates that if just 5–10% of checking balances migrate toward higher-yield products, global deposit profits could decline by 20% or more. Over a decade, profit pools could shrink by $170 billion globally if incumbents fail to reposition.

This dual dynamic — efficiency and erosion — defines AI’s role in digital banking.

Banks that embed AI into governance, compliance workflows, customer journeys, and capital allocation strategies will strengthen resilience. Those that treat AI as a surface-layer chatbot risk structural decline.

Stablecoins, Tokenized Deposits, and the Future of Banking Infrastructure

The monetary layer of digital banking is evolving as rapidly as AI.

The US GENIUS Act of 2025 introduced regulatory clarity around payment stablecoins. Industry forecasts suggest the market could expand from roughly $250 billion today to between $500 billion and $3.7 trillion by 2030.

Deposit migration risk is material. Deloitte estimates that more than $1 trillion in deposits could be vulnerable under certain scenarios.

The potential reconfiguration of deposit funding is not theoretical. Forecast scenarios suggest a material expansion of payment stablecoins that could directly impact traditional bank balance sheets.

Even under conservative assumptions, the stablecoin market could double by 2030. In more aggressive scenarios, it may expand nearly fifteen-fold, fundamentally altering liquidity dynamics, cross-border settlement flows, and the economics of deposit funding.

For digital banks, this raises a strategic question: whether to defend deposit margins, integrate tokenized infrastructure, or participate directly in programmable money ecosystems.

Banks must decide whether to issue stablecoins, custody reserves, process transactions, or develop tokenized deposit alternatives. Unlike payment stablecoins, tokenized deposits remain on bank balance sheets and operate within existing regulatory frameworks.

For institutions bridging fiat and digital assets, integration becomes essential. Infrastructure such as a white label crypto app platform enables regulated connectivity between banking rails and digital asset ecosystems.

Digital banking in 2026 therefore extends into programmable money and tokenized liquidity management.

Digital Banking and the Collapse of Customer Loyalty

Structural change is not limited to infrastructure. It extends to consumer behavior.

McKinsey reports that only 4% of new US checking accounts originate from customer loyalty loops, down from 25% in 2018. Consumers are less loyal, more digital, and increasingly guided by AI tools.

More than half of consumers now use generative AI, and most expect their primary bank to offer comparable functionality. If banks fail to integrate AI-powered personalization into mobile-first journeys, switching behavior accelerates.

Digital banking must therefore compete not only on product breadth but on algorithmic visibility.

Precision marketing, data-driven personalization, and seamless cross-channel continuity are now structural requirements.

Operational Resilience and Financial Crime in the AI Era

Regulation is intensifying in parallel with technological change.

In the EU, DORA elevates operational resilience into binding regulatory obligation. In the US, enforcement actions related to AML and financial crime have increased. AI-enabled fraud accelerates detection challenges.

Banks are expected to consolidate data pipelines, embed explainable AI into monitoring systems, and maintain board-level oversight of third-party risk.

Compliance architecture is no longer an operational cost center. It is a prerequisite for scale.

From Digital Bank to Financial Infrastructure Institution

The most advanced digital banks are evolving beyond consumer brands into infrastructure institutions.

They monetize through embedded finance, API-based distribution, regulated balance sheet access, and programmable treasury capabilities. In this model, banking becomes invisible infrastructure powering SaaS platforms, marketplaces, payroll systems, and digital asset providers.

Launching within integrated environments such as a white-label digital bank platform allows institutions to align regulatory structure, capital strategy, and technological deployment in a coherent operational framework.

Digital banking in 2026 is therefore best understood as financial infrastructure — digitally delivered, AI-enabled, and regulatorily supervised.