How to Create a Digital Online Bank. 10 Things You Need to Know

May 21, 2025

It’s difficult to pinpoint when, specifically, the digital world took upshot and covered every aspect of living without consulting the Internet. Businesses and Enterprises can now function effectively, sell online, and even serve online – it’s all convenient. Anyone can pay for almost everything using the Internet and mobile applications, consequently, it’s no surprise that financial sectors and institutions have begun to emerge in the form of Digital core banking software.

“ Newer technologies are driving the latest round of digital change, such as Blockchain, API Banking, Robotic Process Automation, Artificial Intelligence, and the Internet of Things. It may significantly change the financial environment,” according to the Evolving Drifts in Digital Banking Research.

When these technologies are combined in a solution, businesses can go far deeper degrees of personalisation and better client experience, as well as change banking processes, changing the entire basis of how the banking business functions today.

Let us dive in!

Online Banking Technology – 5 Trends

1. Information Encryption

To start an online bank, engage with internet banking when utilising digital banking to make a transaction. Banks can prevent unwanted disclosure of confidential information by applying sophisticated encrypted communications to data. Maintaining a high level of ciphering makes it impossible to break.

2. Login Security

Many financial sectors consider the login procedure to be a potential security threat as a “Big Grey Area.” Banks tighten up such exercises, through features like transaction timeouts for inactive websites, the ability to disable multiple simultaneous logins, multilayer login protocols, etc. Although these advantages are big, the overall tendency can online banking experiences stronger than ever.

3. Credentials

Replica and misleading websites have recently posed serious issues for consumers of digitalization. Banks are now using accreditation tools to assist clients in avoiding these scams. Clients may be confident in a legitimate banking website rather than a fake site by using an authentication process. Besides this, institutions now provide enhanced Extended Validation Secure Sockets Layer (EV SSL) credentials to ensure that clients are notified of the legitimacy of other domains.

4. Computerized Intelligence

Numerous banks are using machine learning and artificial intelligence technology to anticipate potential abnormalities and questionable tendencies even more on the backside. Data and security processing systems at banking can more effectively define irregularities thanks to Machine learning.

5. Opening an Online Account

Remote online banking registration has grown more commonplace currently because of the epidemic. Bankers have moved from using digital technology just in part to fully digitising the internet banking procedure, making it leisurely for clients to open an account from any location.

Digital Banking Services – Major Types

Starting an online bank is simple with the below-mentioned types.

- Accepting debit and credit cards and distributing virtual card numbers

- Establishing accounts (prepaid card, savings)

- Money transfers

- Obtaining electronic statements, and reviewing balances

- Providing loans for personal, mortgage debt, and commercial purposes, among other things

- Services for deposits and paychecks

- Settling debts

- Upgrading individual data

Read on to the next section to know how to create an online bank that pays off…

How to Start Online Banking? Read on to the Top 10 Steps

1. Target Right Audience

Start online banking by targeting the right audience. Conducting an intended audience study before creating a bank is not a piece of breaking news, but what specific information does market study yield and how can it be helpful is a matter of concern.

Any online banking entrepreneurs would start by asking concerns of this nature, such as what companies their target consumers often use, whether they enjoy or hate about the products, and what concerns they have while utilising the World wide web or making money transfers.

Nevertheless, gathering verifiable facts and doing descriptive statistics are more crucial at this point. You can only do this to introduce a successful business.

Key Tips to follow:

- With an international account, create a brainstorming session and a set of issues that must be addressed.

- Choose a business that does study and statistics if you lack the confidence to complete it yourself.

- Make models that forecast potential customer behaviour.

- Utilize forums and social media sites. You may ask questions, interact with potential clients, and find out about their challenges using electronic banking services, for instance, on Quora.

- Before creating a bank, understand key information about the target viewer’s wants and aspirations, which may be discovered through key demographic analysis.

2. Know Your Competitors

Go with competitors’ strategies to understand how to start a digital bank. Knowing competitors and their tactics is also answered by potential customer analysis. It’s a crucial fact that organisations must be aware of before launching a digital bank.

Key Tips to follow:

- Make a list of standards and a scoring system to assess your rivals

- Examine their advantages and disadvantages to users

- Learn about the technologies and methods competitors employ for goods to sell

- Analyse whether competitors’ clients are satisfied with the current assistance

- Contrast your suggestions for digital banking with those of your rivals.

Effectively develop a digital bank’s perceived value. It helps in understanding why clients should use certain products, and why such products resolve users’ problems and enhance their lives. This can be done by conducting a competitive analysis.

3. Creation of Bank MVP

Starting an internet bank requires MVP. Restricted functions involving a model cannot be an MVP because you wouldn’t have enough information to learn from one. Nor can MMP (Minimum Marketable Product) or MMF (Minimum Marketable Function) can be an MVP, because these are geared at generating income rather than promoting knowledge.

Additionally, while creating a bank, it is an error to place more emphasis on the “least” than the “feasible,” as this doesn’t provide enough data to determine business in a specified geography.

Today, an MVP seems to us an exclusive product edition, enabling us to gather sufficient information about how prospective audiences engage with our sector – rather than a marketing plan.

Key Tips to know:

- Find how customers use the product without being required to fully construct a digital bank

- Swift repairs & changes while having initial capital, efforts, and time to put in

- Assessing the possibility, interoperability, and probability of upcoming software product

4. Pick Among the Latest Business Models

How to create an online bank with its models? Know all four models here.

Aggregators. Distributors of payment institutions from a group of companies are known as an aggregator. If you choose to implement this model and build a virtual financial institution, we may lower the costs associated with producing the assistance, deliver more service types—including financials free services—than a solo money holding can, and give partners commercial bank guidance on making wiser financial verdicts depending n the collected information from having a profitable clientele reach.

Open Platforms. E-banking APIs are the best approaches that increase options for capital acquisition, service commodity exchange, and bias the ratio of partners and users. Remember the existence of four basic platform finance models: licencing, shared, proprietary, & joint venture, when using this model to create a bank solution.

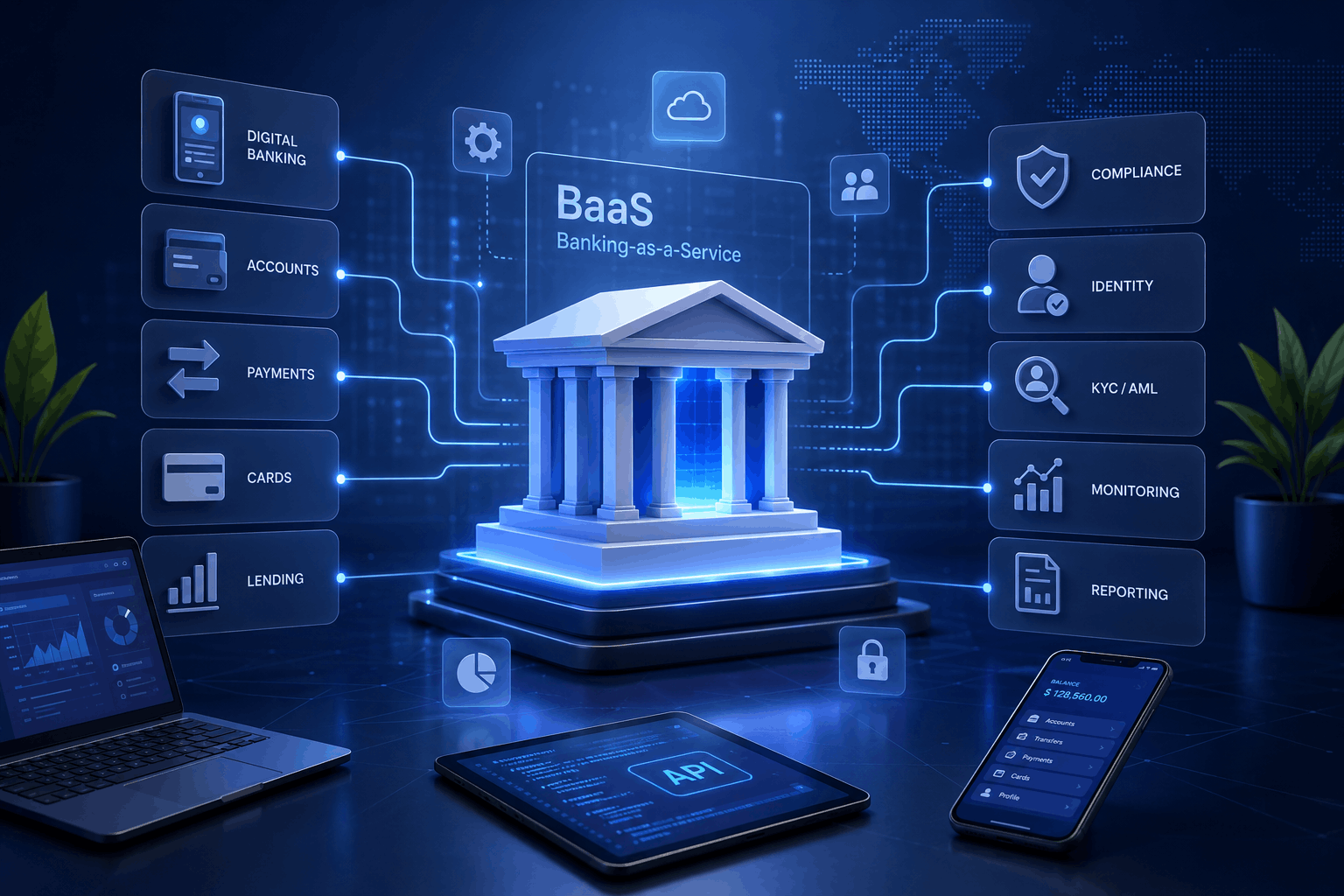

Banking as a Service (BaaS). It is a cloud-based business model that enables internet businesses to function as banks and subsequently obtain the necessary permits. The BaaS model has numerous levels if you’re thinking about expanding a bank using it, including Fintech SaaS, Banking as a Platform (BaaP), Human as a Service (HuaaS) and Infrastructure as a Service (IaaS).

Traditional Universal Banking. A business strategy for conventional banks is to develop online banking facilities, providing all or personal customer services. Typically, it enhances customer service for end users, clients and customers who choose to utilise the Internet with no time to visit the onsite bank in person.

5. Acquire Virtual Banking License

How to create online banking? Another answer is a Virtual License!

Digital Signature. Online identity verification uses a unique code to enable financial services. Learn the procedures to employ a digital certificate under virtual bank authorization as well as how upcoming customers can obtain one.

Digital Environment. The financial system never advances as quickly as online world banking and modules. You must establish a virtual institution that enables customers of a certain bank to follow specified rules.

Key rules to know:

- PSD2 – Payment Services Directive 2

- GDPR – General Data Protection Regulation

- PCI DSS – Payment Card Industry Data Security Standard

- NYSFS – New York State Department of Financial Service

6. Build the NeoBank

Without technically being a typical bank within a legal context, NeoBank is a virtual fintech company that offers standard banking products (loans, deposits, retirement funds, and prepaid cards) and no banking license. To resolve bank technical support issues, it creates an online bank with no permanent offices and seldom any cash registers.

The basic idea of offering financial products in an electronic medium foresees all user needs and addresses them with a few keystrokes, rather than making long, laborious phone calls for customer care or, terrible yet, waiting in line for a “live” adviser.

Key steps to develop:

- Having a well-thought-out concept that is developed into a company concept

- Study of the market and the competition

- Examination of the intended audience

- Selecting a seasoned group of managers and developers

- MVP development (from UX Design prototypes to testing and deployment)

- Organize a gathering of comments

- Correct errors and help

Technology Stack

Technology Stack is an operable architecture of NeoBank. Applications are:

- Liabilities. A banker is a company that offers trustworthy vaults where customers may put their money. This is known as the trust sector. It must convince people they are dealing with a reliable institution.

- Assets. In the business of providing liquidity; a lender must turn a profit from the money it has collected by accurately pricing the fluidity in keeping with the risk character of its customers.

7. Commercial Banking Software

Banking software, often known as core banking applications, provides the framework for developing, implementing, and managing investment vehicles. Moreover, banking software keeps customer information following regional regulations to handle financial transactions and bookkeeping. The appearance and experience of mobile banking, customer self-service portals, online banking, and other consumer engagements are all a result of mobile banking.

Major investment software providers are knowledgeable in both banking and software. They provide design consultation and are aware of financial organizations’ strict compliance requirements. Leading providers of banking software place a strong emphasis on scalability and customization to accommodate unique client interactions and banking offerings.

Essential Features

- Investments and investment products

- Managing information and monitoring history

- Online borrowing

- Online payments

- Portable edition

- Programmable user interfaces

- Real-time client service

- Verification

E-Wallet Solutions

Your consumers may execute smooth transactions everywhere and whenever by starting a digital bank and saving the necessary lending card together with a legitimate excuse once within their e-wallet payment mechanism. A mobile currency offers a variety of payment options, including direct invoicing, QR code reading, and mobile banking transactions.

8. Test for Flaws

Like with any other IT product development, start a digital bank to build and analyse your MVP. MVP, a core LEAN development idea (discussed above), helps you avoid squandering money on stuff your consumers won’t require. In addition, the MVP is essential for evaluating your marketing initiatives as you create a digital bank.

In this situation, the marketing approach should be used first since you need to establish some trust before customers start utilising your product. By releasing an MVP, you may assess the success of your marketing campaigns, the level of public trust in your organisation, and the features users like and dislike.

9. Deploy the Platform

From how to start a bank to deploying software, don’t forget about Agile development. Use Scrum, sprints, and continuous integration, as the working foundation to give your clients the most dependable and effective solutions possible (short iterations).

The planning, stabilisation, development, and deployment phases make up each sprint. Therefore, evaluate before deploying, ensure what must be done, and the resources you require, and plan out your sprint.

Then, developers operate independently to deploy and address problems. The customer no longer frequently engages at this stage. However, you can always use a task management system to keep an eye on things.

10. Update and Scale

The virtual bank business unit should be updated and scaled properly. A digital banking programme still needs to pass the support and maintenance development phases once it is published.

Upgrades and maintenance are typically handled by the contractor with cloud-based banking solutions, and scalability is adaptable. However, you will have to entrust competent DevOps engineers and solution architects with the maintenance of server-based payment systems.

How can We Help you? Quick FAQs…

We know you’re looking for some important questions to be answered. Here are the two most asked questions:

1. How to create your bank in a pocket-friendly manner?

The price of creating a banking app can range from $100,000 to $500,000. But that might go to $1,000,000 when working with an internal team. MVPs could only cost you $100,000, relying on the development team you pick.

2. Which is Better: Beginning from Scratch or Purchasing a Pre-Made Solution for a Financial Institution?

Online bank startup requires new software that can be bought off the shelf or developed from scratch. How you start a bank – off the shelf or scratch building – is a matter of need.

If you have recourse to a significant team of experts, you can build your core banking solution from scratch. You’ll need to spend between $500,001 to $1,000,000 on server fees, staff wages, licencing apps, and API subscriptions throughout this scenario.

However, if you buy an off-the-shelf banking service, you will not be responsible for any of those service fees or admin wages. Instead, you can ask for specific changes to arrive at a one-of-a-kind solution that matches your initial requirements.

This pre-made solution will cost you between $250 000 and $500 000 to purchase and implement in your financial sector.

Starting from scratch with a digital bank could provide you access to state-of-the-art equipment and a lower cost structure, but achieving sustainable economics still requires a fine line to walk. Important decisions and tactics, such as the kind of regulatory licencing, the finest technology providers, and your company strategy, will pave the way for your success.

It takes extensive study, clever influence on firm performance, and careful adherence to regulatory requirements to create digital banking. Additionally, to start a bank put your customers first while taking into consideration their shifting tastes and demands. Also, use caution while selecting the technology and design choices for your potential online bank.

How to develop online banking applications immediately? Get a consultation today!

- Great blog! Your step-by-step guide on creating a digital online bank is clear, practical, and insightful. Really helpful for startups exploring fintech solutions. Keep sharing such valuable content! Finacus Solutions 04.07.2025 01:21 pmReply :